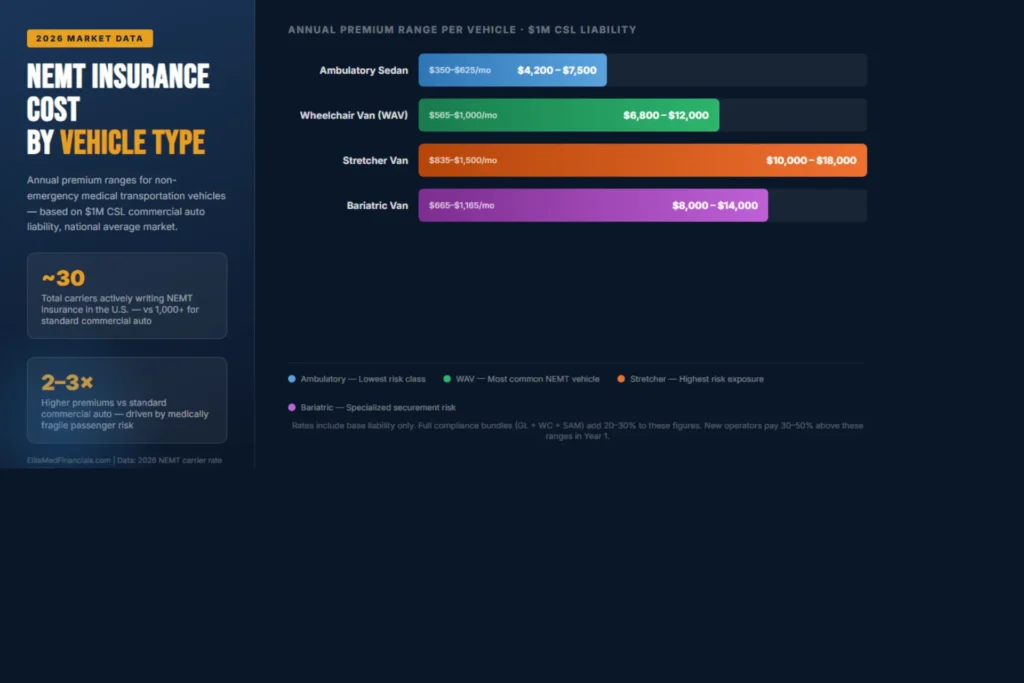

| NEMT Insurance Cost — Quick Answer NEMT insurance costs $4,000–$18,000 per vehicle annually in 2026. Ambulatory sedans average $350–$625/month ($4,200–$7,500/year). Wheelchair-accessible vans (WAVs) run $565–$1,000/month ($6,800–$12,000/year). Stretcher vans exceed $10,000/year. Costs vary by state, fleet size, driver history, and coverage level — new operators pay 30–50% more than established fleets. |

Table of Contents

What Is NEMT Insurance and Why Does It Cost More Than Regular Auto Insurance?

If you’ve just priced out NEMT insurance for the first time, the number probably stopped you cold. A wheelchair van that would cost $1,500–$2,000 a year to insure as a personal vehicle can run $7,000–$12,000 under a commercial NEMT policy. That gap exists for specific, understandable reasons — and once you understand them, you can work with them instead of just paying them.

How NEMT Insurance Differs From Standard Commercial Auto

Standard commercial auto insurance covers vehicles used for business purposes — deliveries, sales calls, contractor work. NEMT insurance is classified as for-hire livery coverage, which means you are transporting paying passengers under a contract, and that changes everything about how insurers assess your risk.

The biggest difference comes down to where coverage stops. A standard commercial auto policy typically ends at the curb. If a passenger is injured inside your vehicle in an accident, you are covered. But if that same passenger falls while you are helping them down a ramp, or while their wheelchair is being secured, a standard policy may deny the claim entirely — arguing it is neither a vehicle accident nor a general liability incident. NEMT policies close this critical gap through loading and unloading endorsements that cover the full door-through-door service your operation actually provides.

For a complete breakdown of what each coverage type requires in your state, see our NEMT insurance requirements guide.

Why Insurers Price NEMT Higher: The Risk Breakdown

In the eyes of an underwriter, you are not just a driver — you are a mobile healthcare facilitator. The passengers you transport are elderly, disabled, or medically fragile. A fender bender that causes a bruise in a 25-year-old can trigger a catastrophic health decline in an 85-year-old dialysis patient. That asymmetry is precisely what drives the non emergency medical transportation insurance cost to 2–3x above standard commercial auto.

Standard auto claims average around $12,000. NEMT injury claims average $150,000 or more. That is a 12x severity gap, and every carrier pricing your policy has to account for it. Add to that the fact that only approximately 30 insurance carriers actively write NEMT coverage — compared to 1,000+ for standard commercial auto — and limited competition keeps premiums structurally high.

Required Coverage Types for NEMT Operations

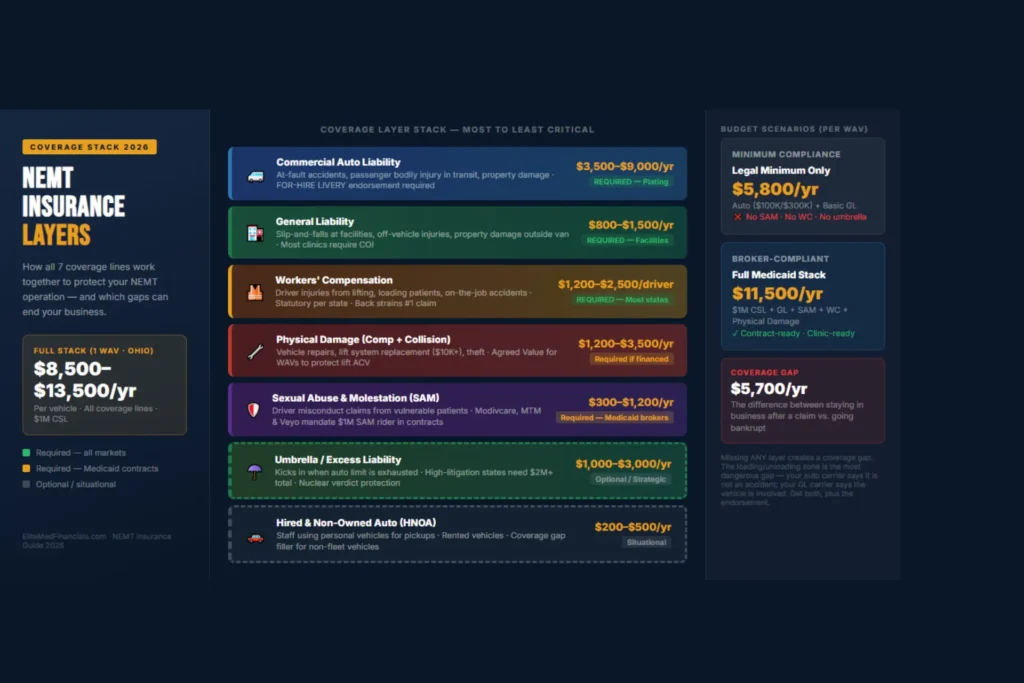

A compliant NEMT insurance stack includes several layers that work together. Missing any one of them can void coverage on a claim:

- Commercial Auto Liability — the anchor, required for plating, typically $1M CSL minimum

- General Liability — covers injuries at facilities and slip-and-falls outside the vehicle

- Workers’ Compensation — mandatory in most states; covers driver injuries from patient lifting

- Physical Damage — required if your vehicle is financed or under Medicaid broker contract

- Sexual Abuse & Molestation (SAM) — mandated by Modivcare, MTM, and Veyo

- Hired & Non-Owned Auto (HNOA) — covers gaps when staff use personal vehicles for work

The true nemt insurance cost for a fully compliant stack runs $8,000–$15,000 per vehicle annually for most operators. That is the number you should budget for — not the stripped-down $4,000 figure sometimes advertised for ambulatory-only, minimum-limit coverage.

NEMT Insurance Cost at a Glance: 2026 National Averages

Here are the verified 2026 figures you need to plan your insurance budget accurately.

NEMT Insurance Annual Cost Estimator

Get a realistic insurance budget range for your NEMT fleet based on 2026 market data. Adjust the inputs below — your estimate updates instantly.

Fleet discount applied automatically at 3+ vehicles

Coverage Cost Breakdown (per vehicle)

| Coverage Line | Est. Annual Cost | Notes |

|---|---|---|

| Adjust inputs above to see your breakdown… | ||

* This estimator provides budget ranges based on 2026 market data compiled from industry sources including carrier rate guides, broker surveys, and RouteGenie/Tobi research. Actual premiums depend on specific vehicle details, driver MVRs, loss runs, and carrier underwriting. Always obtain 3–5 quotes from licensed NEMT specialists before purchasing coverage.

Need help navigating NEMT insurance compliance alongside your billing operations? Elite Med Financials specializes in both.

Get a Free Billing Audit →Average Cost for Ambulatory NEMT Vehicles

Ambulatory sedans and standard passenger vans carry the lowest passenger-handling risk in the NEMT category. They do not require lifts, ramps, or wheelchair securement systems, which keeps liability lower and premiums at the accessible end of the scale:

- Annual range: $4,200–$7,500

- Monthly range: $350–$625

- Geographic spread: Rural $3,500–$4,500 / Large city $5,500–$7,500+

Average Cost for Wheelchair-Accessible Vans (WAV)

Wheelchair-accessible vehicles carry a 15–30% premium over ambulatory vehicles because of the mechanical complexity of lift systems and the liability exposure during securement. A single improper tie-down incident can generate a $100,000–$300,000 claim under the 4-point securement standards required by 49 CFR §571.222:

- Annual range: $6,800–$12,000

- Monthly range: $565–$1,000

- WAV surcharge over ambulatory: $2,600–$4,500/year

Average Cost for Stretcher and Bariatric Vans

Stretcher and bariatric transport vehicles sit at the top of the NEMT risk spectrum. Two-person crews, specialized securement, and the highest injury liability in the event of a sudden stop or ramp failure push these rates significantly higher:

- Stretcher van annual range: $10,000–$18,000

- Bariatric van annual range: $8,000–$14,000

Monthly vs. Annual Cost Reference Table

| Vehicle Type | Monthly Low | Monthly High | Annual Low | Annual High | Avg. Annual |

| Ambulatory Sedan/Van | $350 | $625 | $4,200 | $7,500 | $5,850 |

| Wheelchair Van (WAV) | $565 | $1,000 | $6,800 | $12,000 | $9,400 |

| Stretcher Van | $835 | $1,500 | $10,000 | $18,000 | $14,000 |

| Bariatric Van | $665 | $1,165 | $8,000 | $14,000 | $11,000 |

*Based on $1M CSL commercial auto liability. Bundles with GL and workers’ comp add 20–30% to these base figures. 2026 rates are running 12–15% higher than 2024 levels, driven by rising medical costs, social inflation, and carrier exits.

NEMT Insurance Cost by Coverage Type (2026 Rate Tables)

Commercial Auto Liability Costs

This is the anchor of your entire policy — the coverage required before your vehicles can be legally plated and operated. The NEMT insurance cost for commercial auto liability runs:

- Ambulatory vehicles: $3,500–$6,000/year ($292–$500/month)

- Wheelchair vans: $5,000–$8,500/year ($417–$708/month)

- Stretcher vans: $7,000–$12,000/year

Most Medicaid broker contracts require $1M–$1.5M Combined Single Limit (CSL). If your state minimum is lower, your Modivcare or MTM contract overrides it — and that mandate adds 15–25% to your base premium. For a complete breakdown, our guide on commercial auto insurance for NEMT covers eligibility, limits, and state requirements.

General Liability Insurance Costs

General liability protects your business from injuries and property damage outside the vehicle — at medical facilities, in parking lots, or during patient transfers inside buildings. Most clinics require a COI showing GL before allowing your drivers on-site:

- Annual cost: $800–$1,500

- Monthly: $67–$125

- Required limits: $1M/$2M occurrence/aggregate

Read our guide on NEMT general liability insurance for what this policy does and does not cover in the context of medical transport operations.

Workers’ Compensation Costs

Every NEMT driver faces real physical risk. Back strains from lifting patients and injuries during wheelchair transfers are the most common workers’ comp claims in this industry:

- Annual cost: $1,200–$2,500 per driver

- Monthly: $100–$208 per driver

- High-cost states (CA, NY, FL, TX): 2–4x the national average

Physical Damage Coverage Costs

Physical damage covers vehicle repairs — and for WAVs, that means the $10,000+ lift system as well. Use agreed value coverage for WAVs rather than actual cash value to lock in the lift’s replacement cost:

- Standard van: $1,200–$2,500/year

- Wheelchair van: $1,800–$3,500/year (20–40% more due to lift equipment)

- $500 deductible: +20–30% premium / $2,500 deductible: saves 20–35%

Optional Add-Ons

| Coverage | Annual Cost | When You Need It |

| Hired & Non-Owned Auto (HNOA) | $200–$500 | Staff using personal vehicles for business |

| Sexual Abuse & Molestation (SAM) | $300–$1,200 | Medicaid broker contracts mandate it |

| Umbrella/Excess Liability ($1M layer) | $1,000–$3,000 | Required in high-litigation states |

Full Coverage Package — Real Budget Example (3-Vehicle Ohio Fleet)

| Coverage Item | Calculation | Annual Total |

| Commercial Auto Liability | $6,500 × 3 vehicles | $19,500 |

| General Liability | Flat policy | $1,200 |

| Workers’ Compensation | $2,800 × 3 drivers | $8,400 |

| Physical Damage | $1,500 × 3 vehicles | $4,500 |

| Umbrella ($1M layer) | Flat policy | $2,000 |

| Broker/Financing Fees | Estimated | $1,200 |

| TOTAL ANNUAL BUDGET | $36,800 | |

| TOTAL MONTHLY BUDGET | $3,067 |

The difference between minimum legal compliance ($5,800/vehicle) and a full broker-compliant package ($11,500/vehicle) is a $5,700 gap. That gap represents the coverage that separates operators who stay in business after a serious claim from those who do not.

NEMT Insurance Cost by State: 2026 State-by-State Guide

Where you operate matters as much as what you drive. NEMT insurance premiums can swing 115% between rural low-cost states and major metropolitan markets — before Medicaid broker mandates even enter the picture.

Most Expensive States for NEMT Insurance

California tops the national list. Strict AB5 labor classification rules drive workers’ comp significantly higher than the national average, Medi-Cal contracts require $1M+ CSL, and the litigation environment is among the most plaintiff-friendly in the country. The average nemt insurance cost 2026 california runs $5,500–$9,000 for ambulatory and $7,500–$12,000 for WAVs. Bay Area and LA operators consistently hit the upper range.

New York is the most expensive single market in the country for NEMT. NYC operators frequently end up in the Assigned Risk pool — when few standard carriers will write the risk at all — with WAV premiums of $8,000–$13,000+ statewide and new ventures sometimes paying $15,000–$22,000 in the five boroughs alone. Getting a TLC Base Letter before approaching insurers is required.

Florida is a hard market. No-fault PIP laws, heavy loading-related litigation, and the exit of multiple standard carriers have pushed the nemt insurance average cost in florida to $5,000–$8,500 for ambulatory and $7,000–$11,500 for WAVs. Miami-Dade operators regularly see $13,000+. AI dashcams have become mandatory for many Florida underwriters in 2026 as a prerequisite for coverage.

Texas is more moderate — partial tort reform keeps rates below coastal levels — but high-mileage rural-to-urban transport routes and metro surcharges in Dallas and Houston push nemt insurance cost 2026 texas to $4,500–$7,500 for ambulatory and $6,000–$10,000 for WAVs. Texas HHSC requires active insurance before Medicaid provider enrollment is complete.

Most Affordable States

The most affordable states for NEMT insurance in 2026 are South Dakota ($2,900–$4,700 ambulatory), Iowa ($3,200–$5,000), Nebraska ($3,100–$4,900), and Montana ($3,100–$4,900). Low litigation rates, rural density, and stable insurance markets keep costs near the national floor. These states still require $1M CSL for Medicaid broker compliance — they just deliver it at a fraction of the coastal cost.

How Medicaid Requirements Drive Premiums

Medicaid broker contracts act as a price floor for your insurance. The four major brokers each impose their own requirements across their operating regions:

| Broker | Auto Liability Min. | Required Riders | Primary Regions |

| Modivcare | $1M CSL | GL, SAM, Workers’ Comp | National / East Coast |

| MTM | $1M CSL | Loading/Unloading, GL | Midwest / West |

| Veyo | $1.5M CSL | 24/7 Telematics, SAM | AZ, CT, VA, WI |

| Southeastrans | $1M CSL | Abuse/Molestation rider | GA, AR, MS, TN |

These mandates add 15–25% ($1,000–$2,500 per vehicle) to your base premium. For the revenue side of the equation — what Medicaid actually pays per trip — our state-by-state breakdown of Medicaid NEMT rates by state provides the complementary picture.

Urban vs. Rural Cost Split

| Location Type | Avg. Annual Premium | vs. Rural Baseline |

| Rural | $3,500 | Baseline |

| Suburban | $4,500–$6,500 | +28–86% |

| Urban | $5,500–$9,500 | +57–171% |

| Major Metro | $7,500–$18,000 | +114–414% |

One practical tip worth $2,000/year: your garaging address — not your service area — determines a significant portion of your rate. Moving from downtown Miami to a suburb 20 miles away can save $2,000 per vehicle annually. Never misrepresent your garaging location, however. Material misrepresentation can void coverage and get a claim denied entirely.

State Breakdown Table — Key Markets

| State | Ambulatory/Year | WAV/Year | Min. Liability | Key Cost Driver |

| California | $5,500–$9,000 | $7,500–$12,000 | $1M CSL | AB5, Medi-Cal, litigation |

| New York | $6,000–$10,000 | $8,000–$13,000 | $1.5M CSL | NYC surcharge, Assigned Risk |

| Florida | $5,000–$8,500 | $7,000–$11,500 | $1M CSL | No-fault PIP, hard market |

| Texas | $4,500–$7,500 | $6,000–$10,000 | $1M CSL | High mileage, metro surcharge |

| Illinois | $4,500–$8,000 | $6,000–$11,000 | $1M CSL | Chicago metro density |

| Georgia | $4,000–$7,000 | $5,500–$9,500 | $1M CSL | DCH certification requirements |

| Ohio | $3,500–$6,000 | $5,000–$8,500 | $500K–$1M | Mid-cost suburban market |

| Massachusetts | $4,800–$8,200 | $6,500–$11,000 | $1M CSL | MassHealth mandates |

| Iowa | $3,200–$5,000 | $4,500–$7,000 | $1M CSL | Low litigation, rural density |

| South Dakota | $2,900–$4,700 | $4,200–$6,500 | $1M CSL | Lowest cost nationally |

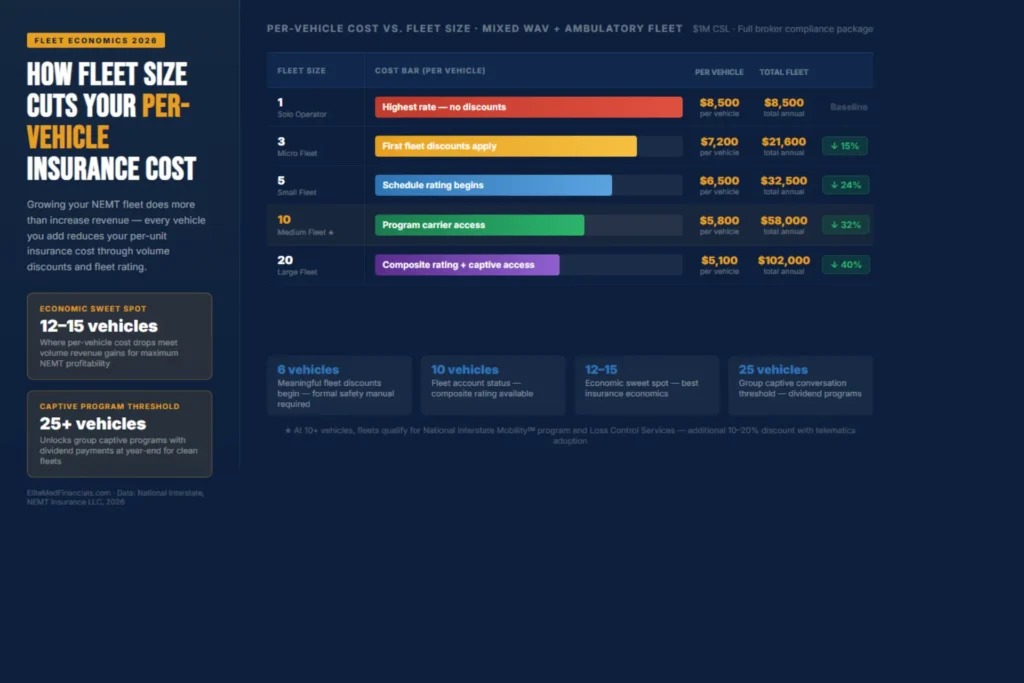

NEMT Insurance Cost by Fleet Size

Your fleet size does not just determine your total premium — it determines your per-vehicle cost. Volume changes the entire conversation you can have with underwriters.

Single Vehicle Operator

Solo operators pay the highest per-vehicle rates in the industry. Without loss history, fleet leverage, or volume discounts, you are manually rated at the absolute maximum for your risk class. You are also entirely dependent on one vehicle and one driver — a single mechanical failure or injury stops your entire revenue. Typical single-vehicle ranges:

- Ambulatory sedan: $4,200–$7,500/year

- Wheelchair van: $6,800–$12,000/year

- No-history surcharge adds 10–20% on top of these ranges

2–5 Vehicle Fleet

At 3 vehicles, meaningful pricing conversations become possible. Multi-vehicle credits of 5–15% apply, and bundling coverages across the same carrier delivers compound savings. A 3-vehicle mixed fleet (2 WAVs + 1 sedan) averages:

- Per-vehicle average: $7,200/year

- Total annual fleet: $21,600

- Discount vs. solo: 15%

6–10 Vehicle Fleet

At 6 vehicles, schedule rating kicks in and underwriters begin assessing your fleet as a whole rather than individually pricing each unit. This unlocks 20–30% per-vehicle savings versus solo rates. A formal written safety program becomes required — not optional — for preferred market access at this tier.

10+ Vehicle Fleet Programs

| Fleet Size | Avg. Per-Vehicle/Year | Total Annual | Discount vs. Solo |

| 1 vehicle | $8,500 | $8,500 | 0% |

| 3 vehicles | $7,200 | $21,600 | 15% |

| 5 vehicles | $6,500 | $32,500 | 24% |

| 10 vehicles | $5,800 | $58,000 | 32% |

| 20 vehicles | $5,100 | $102,000 | 40% |

The nemt insurance cost per vehicle drops progressively as your fleet grows — and that 40% savings at 20 vehicles is one of the strongest financial arguments for scaling your operation. Fleets of 25+ vehicles with strong safety records should explore group captive programs through National Interstate’s Mobility℠ program. For a full capital plan, see our guide on how to start a NEMT business.

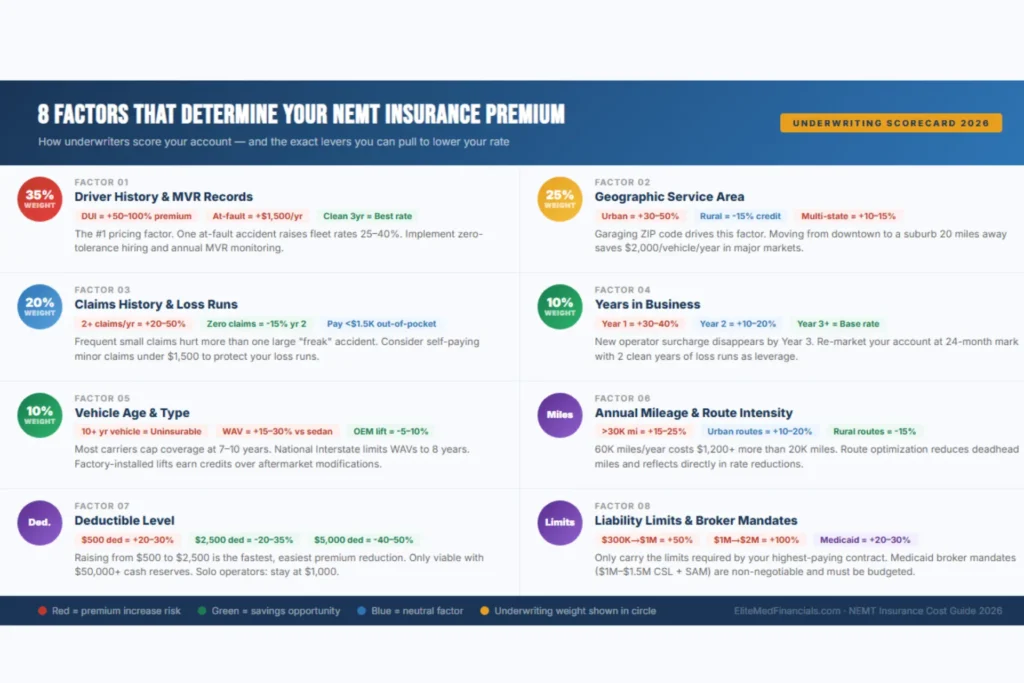

8 Key Factors That Determine Your NEMT Insurance Premium

Understanding how underwriters score your account gives you the power to actively manage your rate instead of just accepting whatever comes back in a renewal quote. These eight factors — and their approximate weights — are the levers you can pull.

1. Driver History and MVR Records — 35% of underwriting weight

Driver records are the single biggest pricing factor in NEMT underwriting. One at-fault accident adds 25–40% to your premium — approximately $1,500+/year per van. A DUI can double your premium or make you uninsurable with standard carriers entirely. Underwriters review 3–5 years of MVR history. Maintaining clean records across your entire driver roster is the most powerful cost-control lever available to you.

2. Vehicle Age and Type — 10% of underwriting weight

Most carriers cap vehicle age at 7–10 years. National Interstate will not write WAVs older than 8 years. Factory-installed OEM lifts earn underwriting credits; aftermarket modifications carry surcharges. A 2026 model with ADAS sensors costs about $800 more annually than a 2020 model — but the safety data those sensors generate often offset that difference within 18 months.

3. Claims History and Loss Runs — 20% of underwriting weight

Underwriters pull 3–5 years of loss runs the moment your application lands on their desk. Two or more claims in a single year, or any claim exceeding $50,000, triggers 20–50% surcharges or non-renewal. A critical strategy: consider paying minor claims under $1,500 out of pocket. A small fender bender on your loss runs costs far more in premium increases over three years than the repair itself.

4. Years in Business — 10% of underwriting weight

New ventures pay 20–40% more than established operators. Progressive surcharges operators under one year by 25%. National Interstate eases requirements at the 3-year mark when experience-rated pricing becomes available. If you are just starting, budget for the new operator penalty and plan to re-shop your coverage at the 24-month mark when you have two clean years to show.

5. Annual Mileage

Declaring 60,000 miles per year versus 20,000 can add $1,200 or more annually per vehicle. Route optimization that reduces deadhead miles is not just good for fuel costs — it reflects directly in your insurance rate. Underwriters verify mileage through odometer logs, GPS data, and ELD records. Never under-report — misrepresentation leads to denied claims.

6. Geographic Service Area

Urban routes add 30–50% over rural baseline rates. Your garaging zip code is one of the first things a carrier checks. Multi-state operations require blanket policies with a 10–15% exposure fee. The gap between downtown Miami and a suburb 20 miles away is $2,000 per vehicle annually. Make sure your declared service area matches your actual operations — discrepancies void coverage.

7. Deductible Level

Raising your physical damage deductible from $500 to $2,500 saves 20–35% on that coverage line. Fleets with 5+ vehicles and $50,000+ in operating reserves should consider $5,000 deductibles for 40–50% savings. Solo operators should stay at $1,000 — the coverage buffer is too important when your entire revenue depends on one vehicle.

8. Liability Limits and Broker Requirements

The difference between $300,000 in liability and $1M costs approximately 50% more in premium. Moving from $1M to $2M adds roughly 100%. When your Medicaid broker contract requires $1.5M CSL in certain states, those requirements override your preference. Understanding this factor before you sign a broker contract can prevent budget-wrecking mid-term surprises.

Why Is NEMT Insurance So Expensive?

| Direct Answer: NEMT insurance costs 2–3x more than standard commercial auto because it covers a mobile healthcare facility, not just a delivery van. The passengers are medically fragile, the equipment is specialized, the liability extends beyond the vehicle, and only ~30 carriers will write this risk at all. |

Medical Liability Exposure

When your passenger is an 85-year-old dialysis patient and your vehicle is in a minor fender bender, the resulting injury claim looks nothing like a standard auto accident. The same collision that causes a bruise in a healthy adult can trigger catastrophic health decline in a medically fragile passenger. Average NEMT injury claims run $150,000–$500,000. Standard auto claims average $12,000–$50,000. That 4–6x severity gap is the core engine behind every premium you pay.

Insurers also account for the liability tail — the fact that injuries in medically fragile passengers can take months or years to manifest fully. The insurance company keeps your premium reserve in place for a decade or more after the policy period ends. You are not just paying for this year’s risk; you are paying for the long tail on today’s transportation.

High-Risk Passenger Profiles

CMS data shows that 65% or more of NEMT passengers are 65+ years old or have significant mobility limitations. These passengers carry pre-existing conditions, fall risks, and medical complications that make even minor transport incidents potentially catastrophic. Insurers apply an Insurance Multiplier Rate of 2–3.5x on accounts transporting this population compared to commercial auto accounts with standard passengers.

Wheelchair and Equipment Liability

Forty to sixty percent of all NEMT claims occur during loading and unloading — not in traffic. A lift failure mid-operation, a wheelchair that tips because of an improper tie-down, or a patient fall at the top of a ramp — these incidents happen with no moving vehicle and no traffic involved. Without a specific loading and unloading endorsement, your auto carrier argues it is not a vehicle incident, your GL carrier argues the vehicle is involved, and you are left in a coverage gap that could put you out of business.

New Operator Surcharges

New operators are, from an underwriter’s perspective, a complete statistical unknown. Without 3 years of loss runs to review, they price for worst case. The data supports that approach: approximately 40% of NEMT startups either fail or have a major claim within their first 18 months. The new operator surcharge of 20–40% is priced risk for exactly that reality — and it dissipates as you build a track record.

Only approximately 30 carriers write NEMT insurance nationwide. When Sentry exited in 2024 due to nuclear verdict exposure, it did not create new competition — it created a capacity vacuum. When you have nowhere else to go, carriers price accordingly. E&S markets now handle 60% of NEMT business at 25–50% above admitted rates.

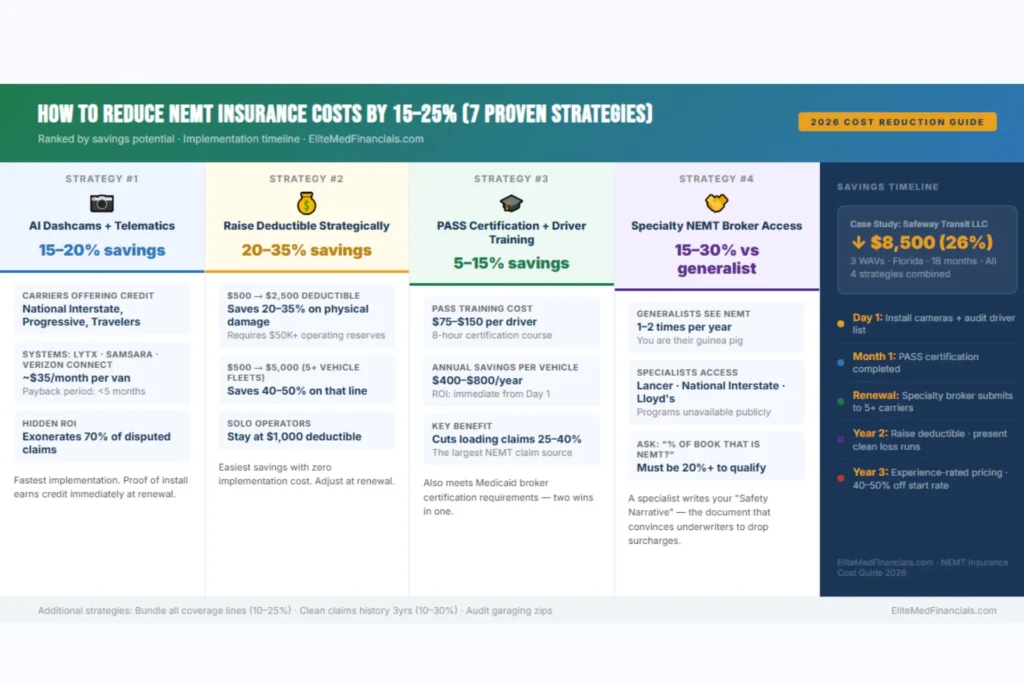

How to Reduce NEMT Insurance Costs by 15–25%

Most NEMT operators leave money on the table at every renewal by treating insurance as a fixed utility rather than a variable they can actively manage. Here are seven evidence-based strategies that produce measurable savings.

1. Install Dual-Facing Dashcams and Telematics — 15–20% savings

Systems like Lytx DriveCam, Samsara, and Verizon Connect Reveal do two things simultaneously: they earn immediate telematics credits of 15–20% from carriers like National Interstate, and they exonerate your drivers in approximately 70% of disputed claims — preventing fraudulent payouts that would raise your rates for years. For a 3-vehicle fleet, telematics costs about $1,260/year and saves approximately $3,600 in premium. Net savings after cost: $2,340. Payback: under 5 months.

2. Get Every Driver PASS Certified — 5–10% savings

PASS (Passenger Assistance, Safety and Sensitivity) is an 8-hour certification that teaches proper securement, patient transfer, and sensitivity protocols. Carriers including Progressive and Travelers offer premium credits for 100% PASS-certified driver rosters. More importantly, PASS certification cuts loading and unloading claims — the source of 40–60% of your total loss exposure — by 25–40%. Cost: $75–$150 per driver. Annual savings per vehicle: $400–$800. Return on investment is immediate.

3. Raise Your Deductible Strategically — 20–35% savings

Raising your physical damage deductible from $500 to $2,500 delivers the fastest, easiest premium reduction in NEMT insurance. If your fleet runs clean and you maintain $50,000+ in operating reserves, moving to a $5,000 deductible produces 40–50% savings on that coverage line. Only do this if your cash position can genuinely absorb a self-insured loss. Solo operators should stay at $1,000.

4. Bundle All Coverage Lines Under One Carrier — 10–25% savings

Separate policies for auto, GL, workers’ comp, and physical damage all carry individual overhead, broker fees, and audit costs. Bundling through a specialty NEMT carrier via a BOP (Business Owner’s Policy) saves 10–25% compared to standalone policies and eliminates the dangerous coverage gaps that form at the boundaries between separate policies — particularly the loading and unloading grey zone.

5. Use a Specialty NEMT Broker — 15–30% savings vs. generalists

A generalist agent sees NEMT accounts once or twice a year. A specialty NEMT broker sees dozens per month and has direct appointments with NEMT-only programs — markets like National Interstate, Lancer, and Berkshire Hathaway Guard — that are unavailable to the general public. They know which safety narrative convinces underwriters to drop surcharges, and they will fight for you at renewal in ways a generalist never will. Ask: “What percentage of your book is NEMT?” If the answer is under 20%, find a specialist.

6. Build Two Years of Clean Claims History — 10–20% savings (cumulative)

Your first clean year drops premiums 15–25% at renewal. A second clean year produces another 10–20%. After three years, the new operator surcharge is gone entirely and you qualify for experience-rated pricing from preferred carriers — 40–50% below your original starting rate. Every small, payable claim you keep off your loss runs is worth more than the claim itself over the next three renewal cycles.

7. Audit Your Driver List and Garaging Zip Codes — immediate savings

Remove occasional drivers with recent violations from your policy — even part-time staff affect your fleet’s risk score. Verify that your garaging addresses reflect where vehicles actually sleep overnight. Re-verify projected mileage to keep declarations accurate. For the compliance side of keeping your operation insurable, our NEMT compliance guide covers what auditors look for and how to stay protected.

Elite Med Financials — NEMT Revenue Cycle Management

Stop Losing Revenue to NEMT Billing Errors

Most NEMT operators lose 12–23% of their billed revenue to claim denials, underpayments, and billing code mismatches. Our specialists recover that revenue — so your insurance investment actually pays off.

- Medicaid & broker contract billing compliance

- Denial management & appeals

- Trip documentation audit support

- NEMT-specific coding & modifier expertise

- Real-time reporting dashboard

- Works with all major NEMT software platforms

No commitment required. Free audit identifies your top 3 billing gaps within 48 hours.

NEMT Insurance Cost for New Businesses: Year 1 Budget Guide

| Hard Truth: You will pay the highest insurance premium of your entire business life in Year 1. Plan for it, then build toward the rates you deserve. |

New operators typically pay $8,000–$12,000 for a single ambulatory sedan and $11,000–$16,000 for a wheelchair van in their first year, compared to $5,500–$8,500 for a 2–5 year established fleet. A 3-vehicle mixed fleet startup can total $22,000–$45,000 in Year 1 insurance alone.

That new operator surcharge of 30–50% exists because underwriters have no loss history to review. Without 3 years of loss runs, you are a statistical unknown — and 40% of NEMT startups either fail or have a major claim within 18 months. The surcharge is simply the actuarial reality of that uncertainty.

Year 1 Budget Example — Single Wheelchair Van, Texas

| Coverage Item | Year 1 Range |

| Commercial auto liability | $7,000–$9,000 |

| General liability | $1,000–$1,500 |

| Workers’ comp (1 driver) | $1,500–$2,000 |

| Physical damage | $1,800–$2,500 |

| TOTAL Year 1 Annual | $11,300–$15,000 |

| Down payment (20%) | $2,260–$3,000 |

| Monthly installments | ~$1,000–$1,100 |

Insurance typically represents 10–15% of total NEMT startup costs. For the complete capital plan — vehicles, licensing, software, and working capital — our guide on total NEMT startup costs breaks down every line item from vehicle acquisition through your first Medicaid enrollment.

Year-Over-Year Premium Reduction Timeline

- Year 1 (no claims): 15–25% reduction at first renewal

- Year 2 (no claims): additional 10–20% reduction (total 30–40% off start rate)

- Year 3: another 10–15% (total 40–50% savings; new operator surcharge fully gone)

To qualify for lower first-year rates, get all drivers PASS certified before your first quote, install telematics on Day 1, and use a specialist broker who can present a Professional Readiness Folder to underwriters. That preparation earns management credits of 5–10% before you have transported a single patient.

If you are in the planning stage, our NEMT business plan template includes a dedicated insurance budget section with Year 1–3 projections built in.

Elite Med Financials — NEMT Web Development

Your NEMT Business Needs a Website That Works as Hard as You Do

Most NEMT operators lose broker referrals and private-pay clients because their website looks unfinished or doesn’t convert visitors into bookings. We build NEMT-specific websites that are SEO-optimized, Medicaid-broker-ready, and designed to generate leads — not just sit online.

- 🚐 NEMT-specific design & messaging

- 📱 Mobile-first, fast-loading performance

- 🔍 Local SEO for “NEMT near me” searches

- 📋 Online trip booking & scheduling forms

- ⚕️ HIPAA-awareness in design & contact forms

- 📊 Conversion-optimized service pages

of NEMT clients who book online say a professional website was their first trust signal before calling.

more private-pay inquiries for NEMT operators with a dedicated, optimized website vs. none.

How to Get an NEMT Insurance Quote (Step-by-Step)

Getting an NEMT insurance quote is not like shopping for personal auto. It is a high-stakes submission process, and showing up to an underwriter’s desk with missing paperwork means getting priced for the unknown — which always costs more than being prepared.

Step 1 — Gather Your Documentation

Prepare a digital folder with everything an underwriter will need: business entity documents (LLC or Corp, EIN), physical garaging address, vehicle details (year/make/model/VIN, lift manufacturer and model, securement systems), full driver roster (names, DOB, license numbers), 3–5 years of MVRs, and any active Medicaid broker contracts showing the required coverage minimums.

Step 2 — Collect Loss Runs If You Have Prior Coverage

If you have had any prior commercial auto coverage, request official loss runs from your current carrier immediately. These reports — not your personal recollection of claims — are what underwriters review. Clean loss runs are your single most powerful negotiating chip. Having them ready demonstrates you are a sophisticated risk, not a first-time applicant hoping for the best.

Step 3 — Contact at Least 3–5 Providers

A mix of 2 specialty brokers plus 1–2 direct carriers gives you proper market benchmarking. Top specialty NEMT brokers include NEMT Insurance LLC, Blake Insurance Group, and TransMed Assurance Group. Direct carriers include Progressive Commercial and National Interstate’s Mobility℠ program. Insureon’s NEMT portal offers instant multi-carrier comparison for initial benchmarking.

Step 4 — Compare on Coverage, Not Just Price

Before accepting the cheapest quote, verify: $1M+ CSL limits, loading and unloading endorsement included, SAM rider present, 30-day COI notice in the policy, primary and non-contributory wording, and no exclusion for door-through-door service. The cheapest quote that lacks any of these endorsements can result in total claim denial — which costs infinitely more than the premium savings.

Step 5 — Ask the Critical Questions

The 10 questions that separate knowledgeable buyers from uninformed ones: “Does this include a loading and unloading endorsement?” “Are my limits compliant with my Medicaid broker contracts?” “What exclusions apply to off-radius trips?” “Does it cover door-through-door service?” “How are SAM claims handled?” “Is there a new driver waiting period?” “What is the carrier’s AM Best rating?” “What telematics earn premium credits?” “How fast are COIs issued?” “How often will we review loss runs to negotiate lower rates?”

Timeline to Expect

Complete applications with clean MVRs receive quote indications in 24–72 hours. Binding typically takes 3–7 days through proper underwriting review. Rush same-day binders are available for licensed operators with clean preliminary MVRs — typically with a 10–20% expedite fee. Incomplete applications cause 50% of quote delays; MVR pulls cause another 20%.

NEMT Insurance Provider Comparison: Top Options in 2026

The right provider depends entirely on your fleet size, operating area, contract requirements, and risk profile. Here is how to navigate the landscape.

When to Use a Direct Carrier vs. a Specialty Broker

Use a direct carrier if you are a solo operator who needs a quote within 24 hours, your drivers have pristine MVRs, and you only need state-minimum coverage. Progressive Commercial is the most accessible option for new ventures nationally.

Use a specialty broker the moment your fleet reaches 3+ vehicles, you need Medicaid broker contract compliance, you require specialized endorsements (SAM, loading/unloading), or you have any element of your risk profile that might make standard carriers hesitate. Specialty brokers have direct appointments with NEMT-only programs unavailable to the public — and they know how to present your risk.

Top NEMT Insurance Providers in 2026

| Provider | Type | Best For | Est. Annual Range | AM Best |

| Progressive Commercial | Direct Carrier | Startups, 1–10 vehicles, 49 states | $3,500–$12,000 | A+ |

| National Interstate (Mobility℠) | Specialty Carrier | Established fleets 5+, captive programs | $4,500–$15,000 | A+ |

| Lancer Insurance | Specialty Carrier | Government/high-limit contracts, 50 states | $4,000–$14,000 | A- |

| Markel Specialty | E&S Carrier | CA/AZ high-risk, flexible limits | $6,000–$20,000 | A |

| NEMT Insurance LLC | Specialty Broker | Telematics-focused ops, 11 states | $4,000–$16,000 | A- |

| Canal Insurance | Regional Carrier | Southeast, Texas, Florida | $4,200–$13,000 | A |

| Insureon | Digital Marketplace | Multi-carrier quote comparison | Market rate | Varies |

Red Flags When Evaluating Providers

- A broker who asks “What is NEMT?” — they will get you the wrong policy

- Policy attempting to classify your vehicles under ‘Delivery/Courier’ code — different risk class, coverage gaps

- No loading and unloading endorsement — the most expensive gap in NEMT coverage

- Carrier rated below AM Best A- — Medicaid brokers will de-fleet you

- Missing SAM rider when you are a Modivcare or MTM contractor

An important 2026 market note: Sentry exited NEMT entirely in 2024, and both Travelers and Progressive have tightened appetite in several states. The list of non emergency medical transportation insurance carriers is shrinking — not growing — which makes working with a specialty broker increasingly important for proper placement. For external reference, the National Association of Insurance Commissioners (NAIC) maintains carrier licensing data by state if you want to verify admitted status before purchasing.

Frequently Asked Questions About NEMT Insurance Cost

How much is NEMT insurance per month?

In 2026, NEMT insurance costs $350 to $1,000 per month per vehicle for most operators. Ambulatory sedans average $350–$625 monthly. Wheelchair-accessible vans run $565–$1,000. Stretcher vans reach $835–$1,500. Rural operators pay toward the lower end; high-density metro operators pay toward the upper end. These figures are for $1M CSL liability — bundles with GL and workers’ comp add $150–$300 monthly.

Why is NEMT insurance so expensive?

NEMT insurance costs 2–3x more than standard commercial auto because it covers medically fragile passengers who generate claim severity 4–6x higher ($150,000+ average vs. $12,000 standard). Add 40–60% of claims occurring during loading and unloading, specialized wheelchair equipment risks, strict Medicaid broker mandates requiring $1M–$1.5M CSL, and only approximately 30 carriers writing this risk class nationwide — and the pricing structure becomes clear.

What is the cheapest NEMT insurance available?

The lowest NEMT rates — $3,500–$4,200 annually — are available to established operators running ambulatory sedans in rural, low-risk states like Iowa or South Dakota. These rates require clean 3-year MVRs, PASS-certified drivers, telematics adoption, and $1,000+ deductibles. Wheelchair vans cannot achieve these floor rates — expect at minimum 15% more for WAV coverage at baseline.

How much does NEMT insurance cost for a new business?

New NEMT operators pay 30–50% more than established fleets in Year 1. Budget $8,000–$12,000 for a single ambulatory vehicle and $11,000–$16,000 for a wheelchair van. A 3-vehicle mixed fleet typically runs $22,000–$45,000 total in Year 1. The new operator surcharge drops progressively — expect 15–25% savings at your first renewal with zero claims.

How much does NEMT insurance cost per vehicle per year?

NEMT insurance in 2026 runs $4,200–$18,000 per vehicle annually depending on type, state, and fleet size. Ambulatory sedans: $4,200–$7,500. Wheelchair vans: $6,800–$12,000. Stretcher vans: $10,000–$18,000. Fleet discounts reduce per-vehicle costs 20–50% at 10+ vehicles. Full bundle with GL, workers’ comp, and physical damage adds 20–30% to these figures.

Does Medicaid affect NEMT insurance cost?

Yes — significantly. Medicaid broker contracts from Modivcare, MTM, and Veyo mandate $1M–$1.5M CSL auto liability plus GL and SAM riders, adding 20–30% ($1,000–$2,500 per vehicle) to base premiums. Non-compliance results in de-fleeting — removal from the broker network — which eliminates your Medicaid-funded trip revenue entirely. These are non-negotiable contract requirements.

How do I get an NEMT insurance quote?

Gather your LLC/EIN documents, vehicle VINs, driver MVRs (3 years clean), and active Medicaid broker contracts. Submit to 2–3 specialty brokers (NEMT Insurance LLC, Blake Insurance Group) plus 1–2 direct carriers (Progressive, National Interstate). Expect indications in 24–72 hours and binding in 3–7 days. Never accept the first quote without comparing at least 3–5 options.

What kind of insurance do I need to transport medical patients?

A compliant NEMT insurance stack requires: Commercial Auto Liability ($1M CSL minimum with for-hire livery endorsement), General Liability ($1M/$2M), Workers’ Compensation (mandatory in most states), Physical Damage, Sexual Abuse & Molestation (SAM) rider, and a Loading and Unloading endorsement. Total annual cost per vehicle: $5,000–$15,000 depending on vehicle type and state.

How much does NEMT insurance cost in Texas?

Texas NEMT insurance averages $4,500–$7,500 annually ($375–$625/month) for ambulatory vehicles and $6,000–$10,000 for WAVs. Dallas and Houston metro surcharges add 15–25% to baseline rates. Texas HHSC requires active insurance before Medicaid provider enrollment is complete. Nemt insurance cost 2026 texas is moderate compared to coastal states due to partial tort reform.

How much does NEMT insurance cost in Florida?

Florida NEMT insurance runs $5,000–$8,500/year for ambulatory and $7,000–$11,500 for WAVs, ranking among the nation’s highest. Miami-Dade operators regularly exceed $13,000 for WAVs. No-fault PIP laws, heavy loading-related litigation, and multiple carrier exits make Florida one of the hardest NEMT markets in the country. The nemt insurance average cost in florida is running 12–15% higher than 2024 levels in 2026.

How much does NEMT insurance cost in California?

California NEMT insurance averages $5,500–$9,000/year for ambulatory and $7,500–$12,000 for WAVs. AB5 labor classification laws drive workers’ comp significantly higher than national averages. Medi-Cal contracts require $1M+ CSL, and carriers must be admitted through CPUC. Bay Area and LA operators consistently hit the upper range. Nemt insurance cost 2026 california is 40–60% above rural national baseline.

Is NEMT insurance worth it?

Yes — without qualification. A single passenger slip-and-fall claim averages $150,000. A catastrophic loading incident can exceed $500,000. Beyond individual claim protection, proper insurance is your license to earn: without it, you cannot sign Medicaid broker contracts, access hospital agreements, or operate legally in most states. At $700/month per vehicle, you are buying protection against financial ruin and access to contracts worth $100,000+ in annual revenue.

▶ What is the average cost of NEMT insurance per month?

The average cost of NEMT insurance per month is $350 to $700 for ambulatory vehicles and $565 to $1,000 for wheelchair-accessible vans, depending on state, driver history, and required liability limits.

▶ How much does it cost to insure a wheelchair van for medical transport?

Insuring a wheelchair van for medical transport typically costs $6,800 to $12,000 per year, or $565 to $1,000 per month, for $1 million in commercial auto liability coverage. New operators and urban fleets pay toward the higher end.

▶ What is the minimum insurance required for NEMT in most states?

Most states require at least $500,000 to $1 million in commercial auto liability for NEMT operations. However, Medicaid broker contracts from organizations like Modivcare and MTM typically mandate $1 million to $1.5 million combined single limit, plus general liability and additional endorsements.

▶ Can I lower my NEMT insurance premium without reducing coverage?

Yes. Installing dual-facing dashcams earns 15 to 20 percent premium credits, PASS certification reduces loading claims by 25 to 40 percent, raising your deductible from $500 to $2,500 saves 20 to 35 percent, and bundling coverage lines saves an additional 10 to 25 percent — all without reducing required liability limits.

▶ How long does it take for NEMT insurance rates to drop for new operators?

NEMT insurance rates typically drop 15 to 25 percent after the first claim-free year, an additional 10 to 20 percent after Year 2, and another 10 to 15 percent after Year 3. By Year 3, the new operator surcharge is fully eliminated and experience-rated pricing from preferred carriers becomes available.

▶ What does NEMT insurance cover that regular commercial auto does not?

NEMT insurance covers loading and unloading incidents, wheelchair securement liability, door-through-door passenger assistance, and sexual abuse and molestation claims — risks that standard commercial auto policies explicitly exclude. These specialized endorsements are the core reason NEMT coverage costs more than regular commercial auto.

Key Data Points — For Research and Citation

| Verified 2026 NEMT Insurance Cost Data National average NEMT insurance cost (2026): $4,000–$18,000 per vehicle annually, with a median of $8,500–$9,400 for wheelchair-accessible vehicles in mixed-density markets. NEMT vs. standard commercial auto: NEMT policies cost 2–3x more due to medically fragile passenger risk, loading/unloading liability (40–60% of all claims), limited carrier availability (~30 carriers), and Medicaid broker mandate requirements for $1M–$1.5M CSL. Underwriting weight factors: Driver MVR history (35%), geographic location (25%), claims history (20%), years in business (10%), vehicle type/safety technology (10%). Carrier market (2026): Approximately 30 carriers actively write NEMT insurance in the U.S. Sentry exited in 2024. 60% of NEMT risks are now placed in E&S markets at 25–50% premium loading above admitted rates. Average NEMT injury claim: $150,000–$500,000, compared to $12,000–$50,000 for standard commercial auto claims — a 4–6x severity differential that drives structural premium loading. |

| Ready to Protect Your NEMT Business? Insurance compliance and billing accuracy work together. A coverage gap creates a claim denial. A billing error creates a revenue loss. At Elite Med Financials, we help NEMT operators stay protected and profitable — from insurance compliance strategy to full revenue cycle management. ▶ NEMT Billing Services | NEMT Website Development | Free Consultation |

Related guides:

Is NEMT a Profitable Business? | NEMT Complete Billing Guide | NEMT Compliance Guide | Best NEMT Software | NEMT Business Plan Template | Driver Qualification Files