What Is NEMT Commercial Auto Insurance?

NEMT commercial auto insurance is a specialized form of for-hire livery coverage that protects vehicles used in non-emergency medical transportation operations. Unlike personal auto insurance — which voids all coverage the moment you use your vehicle for commercial passenger transport — NEMT commercial coverage provides liability protection during patient pickup and delivery, physical damage coverage for your vehicle and its modifications, and medical payments for passengers injured during transport. Coverage also includes increasingly required protections like Sexual Abuse and Molestation (SAM) endorsements that standard commercial auto policies don’t carry. Minimum required liability limits range from $300,000 to $1,500,000 Combined Single Limit (CSL) depending on state Medicaid requirements, DOT thresholds, and the specific broker network you contract with.

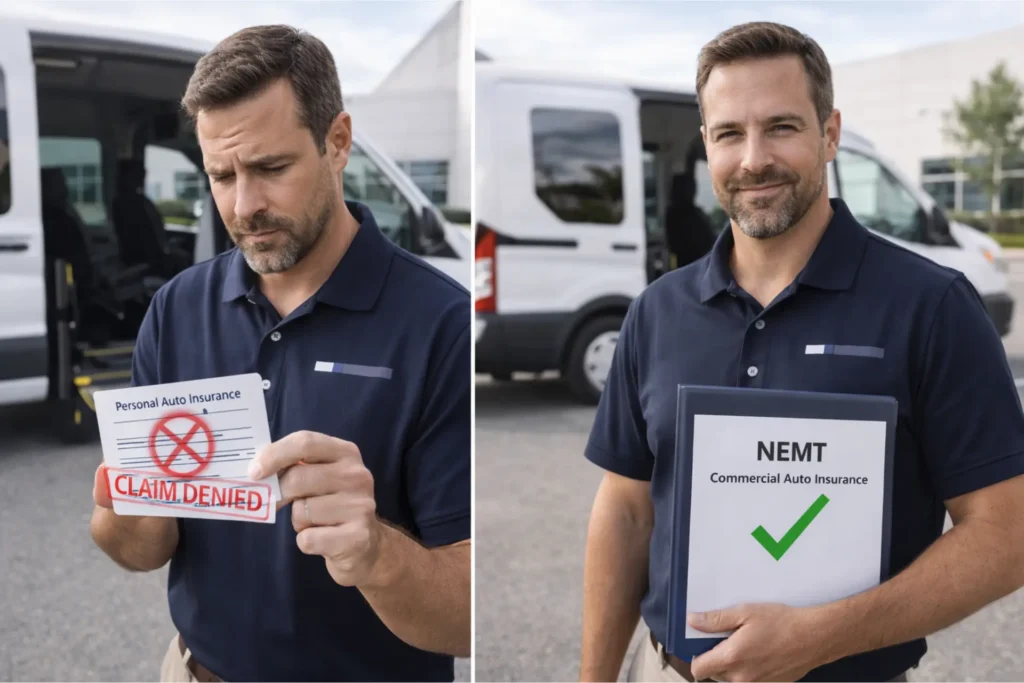

Here’s the situation most new NEMT operators don’t realize until it’s too late: the moment you transport your first Medicaid patient in a vehicle covered only by personal auto insurance, you have no coverage at all. Not reduced coverage. Not partial coverage. Zero. Your personal auto carrier will deny the claim in full, and you’ll be personally liable for every medical bill, every repair, and every lawsuit that follows.

That’s not a scare tactic — it’s the standard exclusion language in every personal auto policy written in the United States. Commercial passenger transport for compensation is explicitly excluded. NEMT operators need NEMT-specific commercial auto insurance, and the requirements go well beyond what most brokers explain when you first inquire.

This guide covers everything: why NEMT requires its own specialized insurance class, the coverage types you actually need, the exact minimum limits your state and broker networks require, what you’ll pay and what drives your premium, which carriers write NEMT, and how to reduce your costs once you’re established.

Before you read this, make sure you’ve looked at our complete NEMT insurance guide — it covers all insurance types a NEMT business needs. This article goes deep on the commercial auto component specifically.

Table of Contents

Why NEMT Requires Commercial Auto Insurance (Not Personal Auto)

Most NEMT startups get this wrong. They have a commercial-looking vehicle. They have a Medicaid contract in progress. They have a business license. And they have personal auto insurance on the van, because their insurance agent said it would be fine for now.

It won’t be fine. It was never fine. And when something goes wrong — a patient falls transferring into the vehicle, a rear-end collision happens en route to dialysis — the claim gets denied and the operator is exposed personally. This happens regularly, and it’s entirely preventable.

The Personal Policy Exclusion That Voids Your Coverage

Every standard personal auto policy contains a commercial use exclusion. The language varies slightly by carrier, but the intent is identical: if you’re using the vehicle for commercial passenger transport and charging for it (or being reimbursed for it through Medicaid), coverage is voided for that trip.

This isn’t a gray area. Personal auto policies were never designed to cover the liability exposure of transporting patients. The moment Medicaid or a broker compensates you for a trip, you’re operating as a for-hire livery service — and personal auto insurance excludes for-hire livery by design.

Some operators ask about commercial endorsements on personal policies. A few carriers offer these, but they’re designed for occasional delivery use — not for regular, scheduled Medicaid patient transport. No endorsement on a personal auto policy adequately covers NEMT liability.

The Medicaid Mandate — Why Commercial Coverage Is a Contract Requirement

Medicaid provider agreements in every state require you to maintain commercial auto insurance as a condition of your contract. This isn’t optional and it isn’t something you phase in gradually — it’s required before you’re authorized to bill your first trip.

The requirement flows down through broker networks as well. ModivCare (formerly LogistiCare), MTM Inc., and every other managed care transportation broker will ask for your Certificate of Insurance (COI) during credentialing. They won’t activate your portal access without it. And they require specifically commercial auto insurance — not personal auto with a note attached.

If your insurance lapses while you’re contracted, your broker network gets an automatic notification from your carrier. Most networks will suspend your trips within 24–48 hours of a lapse notification. Medicaid direct billing access can also be suspended pending proof of active coverage.

For-Hire Livery Classification — Where NEMT Sits in the Insurance World

Insurance carriers categorize risk into classes. NEMT falls into a specific class called for-hire livery — meaning you’re transporting passengers in exchange for compensation. This is the same class that covers taxis, black car services, and paratransit operators.

What makes NEMT more specialized than those classes is the passenger population. You’re transporting elderly individuals, people with disabilities, dialysis patients, and others who require assistive equipment during transport. That passenger profile creates specific liability exposures — including loading and unloading risk and SAM (Sexual Abuse and Molestation) exposure — that standard commercial auto policies don’t address.

This is why major personal lines carriers and even many standard commercial lines carriers won’t write NEMT at all. Progressive Commercial, NEMT Insurance LLC, Prime Insurance Company, National Interstate, and a handful of specialty programs are among the few markets that specifically underwrite this class.

What Happens If You Transport Patients Without Proper Commercial Coverage

The consequences fall into three categories:

Financial: your personal auto carrier denies the claim. You pay out of pocket for any injuries, property damage, medical bills, and legal defense costs. In a serious accident involving multiple patients, this can easily exceed $1 million.

Contractual: your Medicaid provider agreement can be terminated. Your broker network deactivates your account. Any pending claims you’ve submitted get pulled back under review.

Legal: depending on your state, operating commercial passenger transport without proper insurance can result in personal fines, suspension of your DOT number, and in some states, criminal liability.

Personal Auto vs NEMT Commercial Auto — Key Differences

Table 1: Personal vs NEMT Commercial Auto Insurance Comparison

| Coverage Aspect | Personal Auto Policy | NEMT Commercial Auto Policy |

| Passenger transport (for compensation) | Excluded — claim denied | Covered |

| Medicaid trip coverage | Not covered | Covered |

| Loading/unloading patient injuries | Not covered | Covered (with endorsement) |

| SAM coverage | Not available | Available as endorsement |

| Minimum liability limit | State-set (often $30K–$100K) | $300K–$1.5M CSL (Medicaid requirement) |

| Additional insured (broker network) | Not available | Standard practice |

| Certificate of Insurance for credentialing | Not applicable | Provided |

| Driver qualification documentation | Not required | Required by most carriers |

| Claims handling for patient injury | Denies commercial use claims | Full coverage per policy terms |

NEMT Commercial Auto Insurance Coverage Types: What You Need and Why

Not all NEMT commercial auto policies are the same. Standard commercial auto policies cover most risks, but NEMT has specific exposures that require endorsements most general commercial auto policies don’t include by default. Understanding exactly what each coverage does — and what the gaps are — is the difference between being properly protected and having a denial letter when you need coverage most.

Commercial Auto Liability — Your Primary Coverage

Commercial auto liability is the foundation of any NEMT policy. It covers bodily injury and property damage your vehicle causes to others in an at-fault accident. For NEMT, this includes injuries to patients riding in your vehicle, pedestrians struck during transport, and damage to other vehicles.

NEMT policies use either split-limit or Combined Single Limit (CSL) structures. Most Medicaid contracts and broker networks require CSL because it provides more flexible coverage across bodily injury and property damage without separate per-person and per-accident caps.

The typical CSL requirement from broker networks is $1,000,000 — meaning a single occurrence can pay up to $1 million in combined claims. Some high-risk states and specialized routes require $1,500,000 CSL. The bare minimum in most state Medicaid programs is $300,000–$500,000 CSL, but that’s below what ModivCare and MTM require for contracted providers.

Medical Payments Coverage for Passengers

Medical Payments coverage (MedPay) pays for passenger medical expenses regardless of who caused the accident. For NEMT, this is important: your passengers are often elderly, medically fragile, or on Medicaid, and they need immediate medical cost coverage without waiting for liability to be determined.

MedPay is typically offered in limits from $1,000 to $5,000 per person per accident. At $5,000, it’s inexpensive relative to the protection it provides. MedPay pays first, then other coverage responds. Most NEMT specialty carriers include MedPay as standard — verify it’s on your declarations page.

Uninsured and Underinsured Motorist Coverage

Uninsured Motorist (UM) and Underinsured Motorist (UIM) coverage protects you and your passengers when another driver causes an accident but has no insurance or insufficient insurance. Even where it’s optional for commercial vehicles, it matters for NEMT. If an uninsured driver hits your WAV vehicle with three patients aboard, UM coverage pays patient injuries and your vehicle damage when the at-fault driver can’t.

Comprehensive and Collision Coverage

Physical damage coverage includes two components. Collision covers your vehicle’s damage when you hit something or something hits you. Comprehensive covers non-collision damage: theft, vandalism, fire, and weather events.

One critical issue unique to NEMT: Actual Cash Value (ACV) settlement depreciates your vehicle based on age and condition — and it doesn’t separately value your modifications. A hydraulic lift, Q’Straint securement system, and high-roof conversion that cost $15,000 installed could be valued at $4,000–$6,000 under ACV depreciation. Ask your broker specifically about Agreed Value or stated amount coverage for the modification package on any WAV vehicle.

Loading and Unloading Coverage — The Gap Most Operators Don’t Know About

This is the coverage gap that produces the most disputes in NEMT insurance. Loading and unloading describes everything that happens from the moment you exit your vehicle to assist a patient until both of you are securely inside — and again at drop-off.

A patient who trips on the driveway while you’re steadying them isn’t inside the vehicle yet. A patient who falls off a hydraulic lift mid-raise is in between positions. Standard commercial auto liability doesn’t always extend clearly to these exposures — some carriers require a specific endorsement to cover them.

Without this endorsement, a claim for a patient’s hip fracture during boarding could end up in dispute between your commercial auto carrier and your general liability carrier. Always confirm in writing that your policy covers loading, unloading, and transport assistance.

Sexual Abuse and Molestation (SAM) Coverage — Now Essential

SAM coverage was once a nice-to-have in NEMT. In 2026, ModivCare, MTM, and most state Medicaid programs either require it or strongly prefer carriers who include it. NEMT transports vulnerable adults — people who are cognitively impaired, physically dependent, or isolated with a driver for extended periods.

SAM coverage protects your business from claims of inappropriate contact or sexual misconduct alleged against a driver during transport. It doesn’t matter whether the allegation is substantiated — the legal defense cost alone can run $50,000–$200,000. SAM coverage pays those costs.

Typical SAM limits for NEMT range from $100,000 to $1,000,000. The endorsement costs $400–$2,000 annually depending on fleet size and state. It’s one of the highest-value-per-dollar coverages in your entire NEMT insurance package.

Additional Coverages Worth Knowing

Workers’ compensation is required in almost every state if you have W-2 employees. It covers driver medical expenses and lost wages for on-the-job injuries.

Professional liability (E&O) covers claims arising from professional failures — a missed appointment that caused a patient to miss a medical procedure. It’s a growing broker requirement and worth having.

Umbrella/excess liability adds $1M–$5M of protection above your primary policy limits at a fraction of the primary premium cost.

Table 2: NEMT Commercial Auto Coverage Types — What’s Covered, Limits, and Requirements

| Coverage Type | What It Covers | Typical Limit | Required By | Included or Endorsement? |

| Commercial Auto Liability (CSL) | Bodily injury + property damage per occurrence | $300K–$1.5M CSL | All states + all brokers | Included — standard |

| Medical Payments (MedPay) | Passenger medical bills regardless of fault | $1,000–$5,000/person | Recommended | Included on most NEMT policies |

| Uninsured Motorist (UM/UIM) | Damage when other driver is uninsured | Matches liability limit | State-dependent | Included where required |

| Collision | Vehicle damage — your fault or hit-and-run | ACV or Agreed Value | Required if financed | Optional — choose Agreed Value for WAV |

| Comprehensive | Theft, vandalism, weather, fire | ACV or Agreed Value | Required if financed | Optional — always recommended |

| Loading and Unloading | Patient injuries during boarding/exit | Part of liability limit | Recommended | Endorsement — must verify in writing |

| SAM Coverage | Allegations of misconduct by driver during transport | $100K–$1M | ModivCare, MTM, most states | Endorsement — NEMT-specific carriers |

| Workers’ Compensation | Driver injuries on the job | Statutory limits | Required for W-2 employees | Separate policy |

| Professional Liability (E&O) | Missed appointments, documentation errors | $250K–$1M | Growing broker requirement | Separate policy |

| Umbrella/Excess Liability | Coverage above primary policy limits | $1M–$5M | Optional but recommended | Separate policy |

NEMT Commercial Auto Insurance Requirements: State Minimums and Broker Standards

The most important thing to understand about NEMT insurance requirements is this: there are two sets of them. Your state Medicaid program sets a baseline minimum. Your broker network typically requires more than that. You must satisfy both, and the higher standard always wins.

Federal DOT Requirements for NEMT

Federal FMCSA requirements apply when your vehicle crosses state lines for commercial transport or when your vehicle is designed to transport 16 or more passengers including the driver. Most NEMT operators with WAV minivans and standard transport vans are below this threshold and aren’t subject to federal minimums as a primary rule.

If you do cross state lines — transporting a patient to a specialty facility in another state — FMCSA requires proof of insurance filing (Form BMC-91 or BMC-91X) and a minimum of $1,500,000 CSL. You can find the current federal requirements at FMCSA.dot.gov.

For the DOT requirements that affect your specific vehicle type and route structure, see our NEMT compliance guide.

State Medicaid Minimum Coverage Requirements

Table 3: State NEMT Minimum Commercial Auto Insurance Requirements (2026)

| State | Medicaid Agency | Min Auto Liability (CSL) | Min General Liability | DOT # Required | Key Notes |

| Texas | HHSC | $300,000 CSL | $1,000,000 | For qualifying vehicles | Enrollment requires active COI at submission |

| California | DHCS + CPUC | $750,000 CSL (TCP) | $1,000,000 | Yes | TCP permit requires proof of insurance before issuance |

| Florida | AHCA | $300,000 CSL | $1,000,000 | For qualifying vehicles | COPCN required in some counties |

| New York | NYSDOH | $1,500,000 CSL | $2,000,000 | Yes | Article 30 ambulette — highest requirements nationally |

| Virginia | DMAS | $300,000 CSL | $1,000,000 | For qualifying vehicles | COI must name DMAS as additional insured |

| Ohio | ODM | $300,000 CSL | $1,000,000 | For qualifying vehicles | Driver background check required with COI |

| Georgia | DCH | $300,000 CSL | $1,000,000 | For qualifying vehicles | 30-day cancellation notice to DCH required |

| Illinois | HFS | $500,000 CSL | $1,000,000 | Yes | Cook County = high-risk territory, higher market rates |

| Indiana | FSSA | $300,000 CSL | $1,000,000 | For qualifying vehicles | Competitive market with accessible premium levels |

State minimums are the floor, not the ceiling. New York’s $1,500,000 CSL is the highest in the country. Illinois operators in Cook County face both the state’s higher minimum and a market rated as high-risk by underwriters.

Our NEMT insurance cost guide breaks down what operators in high-cost markets typically pay.

Broker Network Insurance Requirements

Table 4: NEMT Broker Network Commercial Auto Insurance Requirements

| Broker | Minimum Auto Liability | Min General Liability | SAM Required? | COI Requirements | Additional Insured |

| ModivCare (LogistiCare) | $1,000,000 CSL | $1,000,000 | Strongly preferred | Must name ModivCare as additional insured | ModivCare, Inc. |

| MTM Inc. | $1,000,000 CSL | $1,000,000 | Required in most states | 30-day advance cancellation notice | MTM, Inc. |

| MAS Transportation (NY) | $1,500,000 CSL | $2,000,000 | Required | Must match Article 30 requirements | MAS Transportation |

| Veyo | $1,000,000 CSL | $1,000,000 | Preferred | Current declarations page + COI | Veyo LLC |

Every major broker in this table requires at least $1,000,000 CSL regardless of what your state sets as minimum. Plan your coverage around the broker requirement, not the state minimum.

What Your Certificate of Insurance Must Show

Your Certificate of Insurance (COI) is the document that proves you have coverage. Getting it right matters — a COI with errors or missing information will delay your credentialing.

Every NEMT COI should include your legal business name, FEIN, coverage types and exact limits (CSL amount, SAM endorsement notation), policy number, effective and expiration dates, carrier name and NAIC number, the broker or state agency listed as Additional Insured with their exact legal name and address, and the 30-day advance notice of cancellation endorsement.

Request one COI for each broker network you work with. If ModivCare requires their legal name in the Additional Insured field, that language must match exactly — “ModivCare, Inc.” not “Modivcare” or “ModivCare LLC.”

States Where NEMT Insurance Is Harder to Find

RLI Transportation explicitly excludes policies domiciled in Connecticut, Kansas, Kentucky, Massachusetts, Montana, North Carolina, Nevada, New York, and West Virginia. If you operate in any of these states, you’re in the E&S (Excess and Surplus) lines market — where non-admitted carriers write coverage that admitted carriers won’t. Work with a broker who specifically specializes in E&S lines transportation insurance.

✅ NEMT Certificate of Insurance (COI) Checklist 2026

Use this checklist before submitting your COI for Medicaid enrollment or broker credentialing. Click each item to mark it complete.

NEMT Commercial Auto Insurance Rates in 2026: What You’ll Actually Pay

NEMT commercial auto insurance costs more than standard commercial auto for reasons we’ll cover in a moment. The range is wide — rural ambulatory operators pay very differently from urban WAV operators in high-risk territories.

Average Annual Premiums by Vehicle Type

Table 5: NEMT Commercial Auto Insurance — Annual Premium by Vehicle Type

| Vehicle Type | Rural / Low Risk | Typical (Suburban) | High Risk (Urban Metro) | Notes |

| Ambulatory sedan/SUV | $3,500–$5,000 | $5,000–$7,000 | $7,000–$10,000 | Lowest risk class in NEMT |

| WAV minivan (Chrysler Pacifica, Toyota Sienna) | $4,500–$6,500 | $6,500–$9,000 | $9,000–$13,000 | Lift/securement = higher liability |

| Full-size WAV (Ford Transit, Ram ProMaster) | $5,500–$7,500 | $7,500–$11,000 | $11,000–$15,000 | Higher capacity = higher premium |

| Stretcher/ambulette van | $6,500–$9,000 | $9,000–$13,000 | $13,000–$18,000 | Highest liability class in NEMT |

| Fleet rate (per vehicle, 3+ vehicles, 2+ yrs) | $3,000–$5,000 | $5,000–$7,500 | $7,500–$11,000 | Fleet discounts at 3+ vehicles |

These are annual premiums for commercial auto liability at $1,000,000 CSL. Adding general liability, workers’ compensation, and SAM coverage brings your total insurance package cost higher — see our NEMT startup costs guide for the complete first-year insurance budget breakdown.

New Operator vs Established Company — The Year-1 Penalty

New NEMT operators pay a significant surcharge in their first year. Insurance carriers rate new ventures as higher risk because there’s no loss history — no claims record to demonstrate safe operation. The new venture penalty typically runs 20–40% above what an operator with 2+ years of clean history would pay.

Table 6: NEMT Insurance Rate Factors and Their Premium Impact

| Rate Factor | Premium Impact | Direction | How to Mitigate |

| New operator (Year 1) | +20–40% surcharge | Upward | Start with clean driving records + full driver training |

| Urban/metro territory | +25–50% vs rural rate | Upward | No mitigation — location is a fixed factor |

| High-risk territory (South FL, Cook County IL, LA County CA, South TX, SF County CA) | +40–75% vs standard metro | Upward | E&S market specialist broker |

| At-fault accident in last 3 years | +30–60% per incident | Upward | Strict MVR policy; remove violating drivers |

| DUI conviction on any driver | +$2,000–$5,000/year | Upward | Mandatory continuous MVR review |

| Vehicle age (10+ years) | +15–30% | Upward | Documented service history helps |

| GPS/telematics monitoring | -5–15% at renewal | Downward | Enroll at policy start, not at renewal |

| Formal safety program | -8–15% | Downward | Document and submit to carrier |

| Claims-free Year 2 | -10–18% vs Year 1 | Downward | Zero at-fault claims Year 1 |

| Claims-free Year 3+ | -20–35% vs Year 1 | Downward | Compound savings from clean history |

| Annual pay in full | -8–13% | Downward | Pay full annual premium at binding |

| Fleet of 3+ vehicles (2+ yrs) | -10–20% per vehicle | Downward | Earns as fleet grows with clean history |

Why Is NEMT Insurance More Expensive Than Regular Commercial Auto?

The vulnerable passenger factor is the primary driver. When a dialysis patient with brittle bones gets hurt in the same accident that would produce a minor claim for a healthy adult, the medical cost and resulting claim are substantially larger. Actuaries build that into NEMT premiums.

The loading and unloading exposure adds a slip-and-fall risk class that doesn’t exist in delivery or contractor fleets. The SAM exposure — a driver alone with a vulnerable adult for extended transport — creates a claim type almost no other commercial class faces. And the litigation climate in states like Florida, California, and Illinois means NEMT injury claims carry higher jury values than comparable accidents in other commercial auto classes.

Top Commercial Auto Insurance Providers for NEMT in 2026

Not every commercial auto carrier writes NEMT. Most decline it entirely. The providers listed here specifically underwrite non-emergency medical transportation.

Specialty NEMT Insurance Programs

NEMT Insurance LLC / Garzor Specialty Division writes NEMT exclusively. Their program covers ambulatory, WAV, stretcher, and ambulette vehicles in approximately 11 states: Alabama, Florida, Georgia, Illinois, Massachusetts, North Carolina, South Carolina, Tennessee, Utah, Virginia, and Oklahoma. Their underwriting is designed specifically for NEMT risks.

National Interstate Insurance has nearly two decades of NEMT and paratransit insurance experience. They offer multiple program structures including Mobility℠ — the first group rental captive designed exclusively for best-in-class NEMT and paratransit operators. A group captive means members pool risk and share in potential financial returns. For an established operator with a clean loss history and genuine safety culture, Mobility℠ is worth investigating.

Amwins/Draco Paratransit Program distributes coverage through wholesale brokers. The program offers admitted paper in approximately 21 states and non-admitted coverage in others. Emergency ambulances, municipal transit agencies, and school transportation are not eligible.

National Carriers Writing NEMT

Progressive Commercial is one of the most accessible national carriers for NEMT through their livery-specific commercial program. Vehicles equipped with lightbars, sirens, or life support equipment are typically ineligible. Their online quoting platform makes them a good first stop for new operators.

Prime Insurance Company is an E&S carrier writing all 50 states. They specialize in hard-to-place risks — useful for operators declined by admitted carriers due to claims history, new venture status, or difficult territory. No minimum premium requirements.

American Business Insurance (ABI) covers over 50,000 commercial vehicles nationwide with an online management portal for real-time certificate issuance, driver changes, and ID cards around the clock.

RLI Transportation writes NEMT through wholesale brokers as E&S non-admitted coverage. They explicitly exclude: Connecticut, Kansas, Kentucky, Massachusetts, Montana, North Carolina, Nevada, New York, and West Virginia. Outside those states, they accept non-preferred risks.

Table 7: NEMT Commercial Auto Insurance Provider Comparison

| Provider | Type | States | Best For | Access Method | NEMT-Specific? |

| Progressive Commercial | Admitted | Select states | New operators, online quote | Direct or agent | Yes — livery program |

| NEMT Insurance LLC / Garzor | Specialty admitted | 11 states | NEMT-exclusive coverage | Through NEMT insurance broker | Yes — NEMT only |

| National Interstate | Admitted + captive | All states | Established fleets, group captive | Wholesale broker | Yes — paratransit expertise |

| Amwins / Draco | Admitted + non-admitted | 21 admitted + others | Growing operators | Wholesale broker only | Yes — paratransit program |

| Prime Insurance Company | E&S non-admitted | All 50 states | Hard-to-place, new ventures | Through licensed producer | No — but writes NEMT |

| RLI Transportation | E&S non-admitted | Most states (excl. 9) | Non-preferred risks | Wholesale broker | Yes — NEMT specialty |

| ABI (American Business Insurance) | Admitted | Nationwide | Tech-forward fleet management | Direct or broker | Yes — NEMT specific |

| Insureon | Marketplace | Nationwide | Quote comparison | Online marketplace | No — aggregator |

How to Compare NEMT Insurance Quotes

Before you call any carrier or broker, gather: driver list with dates of birth and license numbers, vehicle list with VINs and modification details, 4–5 years of loss run reports from your current carrier, your current declarations page, Medicaid provider number, and active broker contracts.

When comparing quotes, verify that loading and unloading is explicitly covered, SAM coverage is included, the COI can name your broker network as additional insured, and the carrier’s AM Best financial strength rating is A- or better.

How to Reduce Your NEMT Commercial Auto Insurance Premiums

NEMT insurance is expensive in Year 1 — that’s unavoidable. But operators who manage the right factors see their premiums drop 30–40% by Year 3 compared to what they paid in Year 1.

Implement a Formal Driver Safety Program First

A documented formal safety program — written policy, driver acknowledgments, regular safety meetings, incident review procedures — demonstrates to carriers that you proactively manage risk. Most NEMT specialty carriers give documented safety programs an 8–15% premium discount.

PASS training and NEMTAC Certified Transport Specialist (CTS) certification for every driver strengthens this further. Some carriers specifically credit NEMTAC certification during underwriting. Beyond discounts, trained drivers produce fewer claims — which is where the real savings accumulate.

Enroll in GPS Telematics Monitoring at Policy Start

GPS telematics systems collect driving behavior data — speed, hard braking, rapid acceleration. Carriers including Progressive Commercial and several specialty NEMT programs offer 5–15% premium reductions for telematics enrollment. Enroll at policy start, not at renewal. Starting at Day 1 means your first full renewal benefits from a full year of data. Samsara and Verizon Connect both have carrier partnership programs.

Pay Your Annual Premium in Full

Most NEMT carriers offer a significant discount for paying the full annual premium at binding. Progressive Commercial’s published data puts this at 13% or more. At a $7,000 annual premium, 13% is $910 in savings — just for paying once instead of monthly.

Maintain Strict MVR Monitoring for All Drivers

One DUI conviction on a driver’s record can add $2,000–$5,000 to your annual premium across your entire fleet. Continuous MVR monitoring catches violations between annual policy reviews. When you discover a violation, you can remove that driver from the policy before renewal — preventing the surcharge from applying.

Shop Your Policy at Every Third Renewal

The market for NEMT insurance shifts. Your risk profile improves as you build loss history. Shopping every 3 years — with 3+ years of clean loss runs in hand — typically produces meaningful reductions. Request competing quotes 90 days before renewal.

Table 8: NEMT Insurance Premium Reduction Strategies

| Strategy | Estimated Savings | Timeline | Difficulty | Notes |

| Formal safety program | 8–15% | Immediate (document before binding) | Medium | Written policy + driver acknowledgments |

| GPS telematics enrollment | 5–15% at renewal | Start Day 1 | Low | Full-year data needed for discount |

| Annual pay in full | 8–13% | Immediate | Low | Most impactful low-effort strategy |

| Continuous MVR monitoring | Prevents 30–60% surcharges | Ongoing | Low | Prevents increases, not just earns discounts |

| Clean claims history Year 2 | -10–18% vs Year 1 | 12 months | Ongoing | Most important Year 2 financial metric |

| Clean claims history Year 3 | -20–35% vs Year 1 | 24–36 months | Ongoing | Compound effect of clean years 2 + 3 |

| Higher deductible (3+ vehicles) | 10–20% | At renewal | Medium | Only when cash reserves support it |

| Fleet size (3+ vehicles, 2+ yrs) | 10–20% per vehicle | As fleet grows | Long-term | Fleet rates with clean history and volume |

The cumulative effect of doing all of this right is significant. An operator paying $8,500/year in Year 1 who implements telematics, completes safety training, pays in full, and maintains zero claims should expect to pay $5,500–$6,500 by Year 3. Over three years, that’s $6,000–$9,000 in total savings on a single-vehicle operation.

For operators managing the billing side of NEMT alongside insurance, see our NEMT billing guide — the same principle applies: correct processes in Year 1 compound into significant financial advantages by Year 3.

NEMT Commercial Auto Insurance: Frequently Asked Questions

What commercial auto insurance do NEMT providers need?

NEMT providers need commercial auto liability insurance with a minimum $1,000,000 CSL, classified specifically as for-hire livery or NEMT transport. The policy must include a SAM endorsement, loading and unloading coverage, and a Certificate of Insurance that names your broker network as additional insured. State minimums range from $300,000 to $1,500,000 CSL, but broker networks including ModivCare and MTM require $1,000,000 CSL regardless of what your state sets.

How much does commercial auto insurance cost for NEMT?

NEMT commercial auto insurance costs $3,500–$9,000+ per vehicle per year for a single-vehicle operator in 2026. New operators in suburban markets typically pay $6,000–$9,000 in Year 1. Established operators with 3+ years of clean claims history pay $4,000–$7,000 for comparable coverage. Urban operators in high-risk territories pay toward the higher end.

Does personal auto insurance cover NEMT driving?

No. Personal auto insurance explicitly excludes commercial passenger transport. The moment you transport a Medicaid patient for compensation, your personal policy provides zero coverage for any claim from that trip. NEMT commercial auto insurance is required before your first trip runs.

Do I need DOT-specific insurance for NEMT?

Most NEMT operators don’t face federal FMCSA requirements directly because most NEMT is intrastate and most vehicles carry fewer than 16 passengers. If you cross state lines or operate vehicles designed for 16+ passengers, FMCSA requires a minimum $1,500,000 CSL and insurance filing on Form BMC-91. Check your vehicle GVWR and route structure, and consult your broker if you’re near the threshold.

Is it cheaper to insure a NEMT vehicle through an LLC?

Forming an LLC changes your legal structure but doesn’t reduce your commercial auto insurance premium. Insurance carriers rate the risk based on your driver pool, vehicle type, geographic territory, and claims history — not your corporate structure. Your premium is the same as an LLC or sole proprietor.

Quick Answers About NEMT Commercial Auto Insurance

What insurance do I need to start a NEMT business?

To start a NEMT business, you need commercial auto insurance with at least $1,000,000 Combined Single Limit (CSL) liability coverage classified as for-hire livery or NEMT transport. You also need general liability insurance at $1,000,000/$2,000,000 occurrence/aggregate limits, a SAM endorsement, and workers’ compensation if you have W-2 employees. All coverage must be in place and reflected on a Certificate of Insurance before you can complete broker credentialing or activate your Medicaid provider account.

How much does NEMT vehicle insurance cost per month?

NEMT vehicle insurance costs approximately $300–$750 per vehicle per month. An ambulatory sedan in a suburban market runs $300–$500/month. A WAV minivan in the same market runs $500–$750/month. Urban and high-risk territory operators pay toward the higher end. These figures represent commercial auto liability at $1,000,000 CSL — total monthly insurance budget including general liability and SAM coverage will be higher.

Why do NEMT providers need commercial auto insurance?

NEMT providers need commercial auto insurance because personal auto policies exclude all coverage for commercial passenger transport. Additionally, Medicaid provider agreements and all major broker networks — including ModivCare and MTM — require proof of commercial auto insurance before credentialing. Operating without it creates personal financial liability, Medicaid contract risk, and legal exposure.

What is the minimum liability insurance for NEMT?

The minimum liability insurance for NEMT is $300,000 CSL at the state Medicaid floor in most states, but all major broker networks require $1,000,000 CSL as their contract minimum. New York requires $1,500,000 CSL under Article 30 ambulette authorization — the highest state-level requirement in the country. Plan for $1,000,000 CSL as your working standard regardless of which state you operate in.

Can I use the same insurance policy for multiple NEMT vehicles?

Yes. Most commercial auto carriers allow multiple vehicles on a single fleet policy. Fleet policies simplify administration — one renewal date, one carrier, one broker relationship. Fleet rates per vehicle also tend to be lower than individual vehicle rates once you have 3+ vehicles and 2+ years of clean claims history.

Which insurance companies write NEMT commercial auto?

Carriers that specifically write NEMT commercial auto include Progressive Commercial (livery program), NEMT Insurance LLC / Garzor (specialty, 11 states), National Interstate (paratransit expertise, all states), Amwins/Draco (wholesale broker, 21 admitted states), Prime Insurance Company (E&S, all 50 states), RLI Transportation (E&S, most states), and ABI nationwide. Most standard carriers like State Farm, Allstate, and GEICO don’t write NEMT at all — work with a broker who specializes in this class.

NEMT Commercial Auto Insurance 2026: Key Facts for Researchers

NEMT commercial auto insurance is classified as for-hire livery coverage — a specialized insurance class distinct from standard commercial auto, taxi, rideshare, or ambulance insurance. It covers vehicles transporting patients to medical appointments on a pre-arranged, compensated basis.

Personal auto insurance explicitly excludes commercial passenger transport. NEMT operators cannot legally rely on personal auto coverage for any Medicaid trip. A claim denial and personal liability exposure result from any accident occurring on a trip covered only by personal auto insurance.

Medicaid provider agreements in all states require active commercial auto insurance as a condition of enrollment. Broker networks including ModivCare and MTM require a minimum $1,000,000 Combined Single Limit (CSL) commercial auto policy and a Certificate of Insurance naming the broker as Additional Insured before portal activation.

New York requires the highest state-level minimum in the country: $1,500,000 CSL under Article 30 ambulette authorization, enforced by the New York State Department of Health.

Annual commercial auto insurance premiums for NEMT vehicles range from $3,500 to $15,000+ per vehicle in 2026, depending on vehicle type, geographic territory, driver history, and operator experience. New operators pay a surcharge of 20–40% above established operator rates due to absence of loss history.

SAM (Sexual Abuse and Molestation) coverage is now required or strongly preferred by ModivCare, MTM, and most state Medicaid programs for NEMT operators. Typical SAM coverage costs $400–$2,000 annually.

RLI Transportation explicitly excludes writing policies in Connecticut, Kansas, Kentucky, Massachusetts, Montana, North Carolina, Nevada, New York, and West Virginia.

GPS telematics monitoring reduces NEMT commercial auto premiums by 5–15% at renewal. Operators who implement a formal safety program, complete NEMTAC driver certification, and maintain zero at-fault claims for 3 consecutive years typically see total premium reductions of 30–40% compared to Year 1 rates.

Published by EliteMed Financials — elitemedfinancials.com | NEMT Billing, Revenue Cycle Management, and Healthcare Web Development