General liability insurance for NEMT protects your business against third-party claims for bodily injury, property damage, and personal injury that occur outside vehicle operation. Unlike commercial auto insurance, which covers vehicle collisions and in-vehicle incidents, general liability addresses the risks that happen on the ground—at patient homes, medical facilities, or during loading and unloading. For NEMT operators, this distinction is critical because a single slip-and-fall claim can cost $50,000–$150,000 or more, and nearly all state Medicaid programs and major broker networks (MTM, ModivCare, MAS, Alivi) require a minimum of $1,000,000 per occurrence and $2,000,000 aggregate general liability coverage as a condition of provider enrollment. Operating without this coverage is not optional—it’s a legal and financial necessity.

For a comprehensive overview of all NEMT insurance requirements, see our complete NEMT insurance guide.

Table of Contents

What Does General Liability Insurance Cover for NEMT?

General liability insurance covers three distinct categories of third-party claims that arise outside your vehicle. Understanding what falls under each category helps you recognize when your GL policy responds versus when other insurance (auto, workers’ comp, E&O) takes over.

Bodily Injury Claims (Slip and Fall at Pickup)

The most common general liability claim in NEMT is a bodily injury incident occurring outside your vehicle. Imagine a patient on crutches exits your van at their residence and slips on a wet driveway. The patient falls, fractures their wrist, and requires emergency room treatment and surgery. Your general liability insurance covers this incident because the bodily injury occurred outside the vehicle and wasn’t caused by vehicle operation. This includes the patient’s medical bills, emergency room costs, surgery expenses, lost wages during recovery, pain and suffering damages, and your legal defense fees if the patient sues. Industry data shows that typical slip-and-fall settlements in NEMT environments range from $30,000 to $100,000, with severe incidents involving fractures, hospitalization, or long-term disability often exceeding $100,000. Your commercial auto insurance will not cover this claim because the injury did not involve the vehicle itself. This is the critical coverage gap that general liability is designed to fill.

Property Damage Claims

While transporting patients, your equipment and your driver’s movements can sometimes damage property at patient homes or medical facilities. A stretcher catches the corner of a doorframe, leaving a visible dent. A wheelchair accidentally scrapes the wall of a narrow hallway at a dialysis center. These incidents trigger property damage claims under general liability. Your GL policy covers the cost of repairs—whether that’s repainting a wall, replacing a damaged doorframe, or repairing flooring. Typical property damage claims in NEMT range from $5,000 to $50,000 depending on the facility and the extent of the damage. However, it’s important to note that standard general liability policies typically do not cover damage to the patient’s own durable medical equipment (like wheelchairs, walkers, or oxygen tanks). That equipment usually belongs to the patient or a medical equipment supplier, and damage to it would require a separate Inland Marine or Cargo endorsement on your policy.

Personal and Advertising Injury

Personal injury in insurance terms doesn’t mean physical harm—it means intangible harms like defamation, privacy violations, or false statements. Imagine a driver mentions to a facility manager that a specific patient “never pays their bills” or “is faking their injury,” and the patient overhears this conversation. If the patient files a lawsuit alleging that their reputation was harmed, your general liability policy’s personal injury coverage responds. This includes legal defense costs and any settlement. Similarly, if your marketing materials make false claims about your coverage territory, service quality, or network participation, and a patient or competitor sues for misleading advertising, GL covers the defense and settlement. While personal injury claims are less frequent than bodily injury or property damage claims, they can still cost $10,000–$50,000 or more in legal fees and settlements, especially if the privacy violation involves health information.

What General Liability Does NOT Cover

Understanding the boundaries of GL coverage prevents costly surprises. General liability explicitly does not cover vehicle collisions or accidents. If your van hits a parked car in a hospital parking lot, injuring the vehicle’s owner, that claim falls entirely under under commercial auto liability, not GL., not GL. Similarly, GL does not cover professional negligence or malpractice claims. If a patient alleges that your driver failed to transport them on time, resulting in a missed critical medical appointment, that falls under Errors & Omissions (E&O) or Professional Liability insurance, not GL. Employee injuries to your own drivers or staff are the domain of workers’ compensation insurance, not GL. And finally, intentional or criminal acts are excluded from nearly all GL policies. If a driver intentionally harms a patient or steals property, no insurance policy covers that—and there’s potential for personal criminal liability.

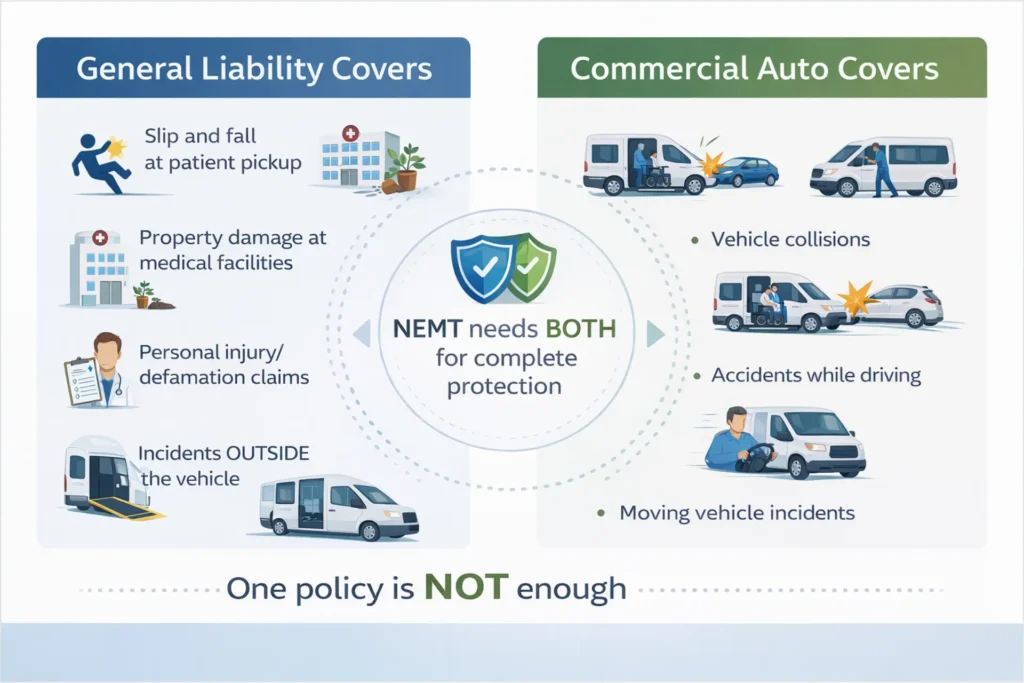

Why NEMT Needs Both Auto and General Liability

One of the most dangerous mistakes NEMT operators make is assuming a single insurance policy covers all liability. Many operators buy only commercial auto insurance, thinking it’s the “catch-all” for transportation liability. Others buy only general liability, believing it handles all their business risks. Both assumptions are wrong, and both leave significant coverage gaps that can bankrupt a business.

The Coverage Gap Between Policies

Commercial auto insurance and general liability insurance sit side by side in your coverage stack, but they protect different risk zones. Commercial auto covers what happens while you’re driving—vehicle collisions, accidents, in-vehicle injuries, and property damage caused by the moving vehicle. General liability covers what happens outside the vehicle—slips, falls, property damage at facilities, and premises-related claims. There’s a distinct “handoff zone” between them, and if you don’t understand this boundary, you end up uninsured for one category or the other.

Here’s the real-world handoff: A patient slips on a wet driveway at pickup before entering your van. That’s a GL claim. Your auto policy doesn’t respond because the vehicle wasn’t involved. A patient is injured when your van hits a parked car. That’s an auto claim. Your GL policy doesn’t respond because the vehicle caused the injury. A gurney damages a clinic doorway during loading. That’s a GL claim arising from your operations outside the vehicle. A collision injures a passenger inside your van. That’s an auto claim. Neither policy substitutes for the other, and operators who carry only auto or only GL end up facing $30,000–$150,000 in uninsured loss when a claim falls outside their single policy’s scope.

Real NEMT Claims Examples

Understanding how each policy triggers in real situations removes the guesswork. In the first scenario, a patient slips on an icy driveway while walking to your van. Your GL policy covers this claim up to $50,000–$100,000 or more, including medical bills and pain-and-suffering damages. Your auto insurance denies this claim because the vehicle wasn’t the proximate cause. Without GL, you’re personally liable for the entire amount.

In the second scenario, your van hits a parked car in a medical facility lot. Your auto liability policy covers this—typically $20,000–$50,000 in property damage and any bodily injury to the vehicle’s owner. Your GL doesn’t respond because vehicle collision is auto’s responsibility. Without auto, you’re uninsured.

In the third scenario, while unloading a stretcher, your driver accidentally smashes a clinic’s glass door. Your GL covers this property damage claim, often in the $5,000–$20,000 range. Your auto policy doesn’t respond because the door damage didn’t involve vehicle operation. Without GL, you pay 100% out of pocket.

In the fourth scenario, a passenger is severely injured when your van accelerates too quickly, causing them to hit their head. Your auto liability responds as the primary coverage. But if the medical costs and pain-and-suffering damages exceed your auto limit ($1,000,000), your GL or umbrella policy can act as secondary coverage, absorbing the excess. Without both policies, you’re exposed above your auto limit.

How Combined Coverage Protects You and Bundling Savings

Think of auto and GL as two overlapping safety nets. They protect different zones, but together they provide comprehensive coverage across all operating scenarios. A $1,000,000 commercial auto policy handles collision and in-vehicle injury scenarios up to its limit. A $1,000,000/$2,000,000 GL policy handles premises and facility scenarios up to its limits. If a major accident occurs where a passenger is severely injured, your auto policy provides primary coverage. If that claim exceeds your $1,000,000 auto limit, your GL or umbrella policy can act as a secondary safety net, covering the excess.

Beyond protection, bundling GL with commercial auto saves significant money. Instead of paying separate brokers and carriers, you consolidate with one company and save 15–25% on total premium. A small operator might pay $3,500–$6,000 for auto only and $800–$2,500 for GL separately, totaling $4,300–$8,500. Bundled with one carrier, that same coverage typically costs $4,500–$7,500 annually—saving $500–$2,000 per year without reducing protection. For larger fleets, bundling savings can exceed $3,000–$5,000 annually.

Most importantly, every major Medicaid network—MTM, ModivCare, MAS, and Alivi—explicitly requires both policies as a condition of provider enrollment. Carry only one, and they’ll deny your application or terminate your contract. This isn’t a matter of choice; it’s a regulatory baseline for accessing Medicaid revenue.

For a detailed breakdown of all insurance costs including both policies, see our complete NEMT insurance cost guide.

Required General Liability Coverage Amounts for NEMT

While Medicaid law doesn’t write a single federal formula for GL limits, nearly every state Medicaid program and broker network converges on the same standard: $1,000,000 per occurrence and $2,000,000 aggregate. Understanding why this is the baseline, and how it varies by network, is essential for compliance.

State Medicaid Minimums

Most state Medicaid agencies have adopted $1,000,000 per occurrence and $2,000,000 aggregate as the de facto NEMT GL requirement. This limit provides enough protection to absorb typical slip-and-fall claims ($50,000–$150,000) and facility property damage ($5,000–$50,000) without forcing every small operator into a prohibitively expensive higher-limit policy. However, some states exceed this baseline. New York, for example, often requires $1,500,000 or $2,000,000 GL for providers operating under Article 30 ambulette rules. California and Texas sometimes push operators toward higher limits for high-volume or high-acuity services. Your first step is to contact your state’s Medicaid agency or Department of Transportation and request their current NEMT coverage requirements in writing. Different states may have different minimums, and using an outdated number could delay enrollment or trigger compliance issues during an audit.

Our complete NEMT insurance guide covers state-by-state variations and network-specific requirements in detail.

MTM Requirements

Medical Transportation Management (MTM), one of the largest Medicaid NEMT brokers nationally, requires $1,000,000 per occurrence and $2,000,000 aggregate GL. MTM also specifies that your general liability deductible cannot exceed $1,000—any higher deductible typically requires special underwriting review and approval. MTM requires your Certificate of Insurance to follow their specific format and wording, with MTM named as an additional insured and loss payee. This formatting requirement is stricter than many operators realize; a certificate that omits the “additional insured” clause or lists MTM’s name incorrectly can trigger a compliance rejection in MTM’s portal. For small operators, MTM-compliant GL typically costs $800–$1,200 per year when bundled with commercial auto.

ModivCare Requirements

ModivCare, another major Medicaid NEMT broker operating in multiple states, also requires $1,000,000 per occurrence and $2,000,000 aggregate GL. Unlike MTM, ModivCare explicitly allows claims-made GL policies, provided you document a clear tail coverage plan or retroactive coverage strategy. ModivCare permits GL deductibles ranging from $1,000 to $2,500, offering more flexibility than MTM’s strict $1,000 cap. For larger fleets or higher-risk operations, ModivCare often recommends—but doesn’t mandate—a $1,000,000 umbrella policy sitting above GL and auto. Typical ModivCare-compliant GL costs $1,000–$1,500 annually for small operators, slightly higher than MTM due to the slightly more permissive deductible range and claims-made option.

MAS Transportation and Alivi Requirements

MAS Transportation, particularly dominant in New York markets, often requires the $1,000,000/$2,000,000 GL baseline but adds a critical requirement: a Hired and Non-Owned Auto (HNOA) endorsement. This endorsement extends your GL and auto coverage to protect situations where employees use personal vehicles for business—for example, when a driver uses their own car to make an urgent patient pickup. Without HNOA, these employee-vehicle incidents create a coverage gap. MAS also pays close attention to umbrella coverage for larger fleets; many MAS contracts encourage or expect operators with 10+ vehicles to carry a $1,000,000–$5,000,000 umbrella policy.

Alivi, a newer but increasingly strict Medicaid broker, requires the same $1,000,000/$2,000,000 GL baseline but mandates a Sexual Abuse and Molestation (SAM) rider—a non-negotiable addition that covers allegations of abuse or misconduct during transport. The SAM rider typically costs $200–$400 annually but is a hard requirement for Alivi enrollment, especially for operators transporting pediatric or developmentally disabled populations. Alivi also enforces tighter deductible controls and certificate-of-insurance formatting requirements, treating them as non-negotiable barriers to enrollment.

Network Compliance Comparison

| Network | GL Minimum (Per Occurrence / Aggregate) | Max Deductible | Key Requirement | Estimated Annual Cost |

|---|---|---|---|---|

| State Medicaid | $1M / $2M | Varies | Varies by state | $800–$2,500 |

| MTM | $1M / $2M | $1,000 | COI formatting exact | $800–$1,200 |

| ModivCare | $1M / $2M | $2,500 | Claims-made allowed with tail | $1,000–$1,500 |

| MAS | $1M / $2M | $2,500 | HNOA endorsement required | $1,200–$1,500 |

| Alivi | $1M / $2M | $2,500 | SAM rider required | $1,200–$1,700 |

The critical lesson is this: before you purchase a general liability policy, contact your target Medicaid networks directly and request their current GL requirements in writing. Don’t rely on outdated information or assumptions. One missing endorsement or incorrect coverage limit can mean contract rejection, enrollment delays, or immediate deactivation if discovered during an audit.

How Much Does NEMT General Liability Cost?

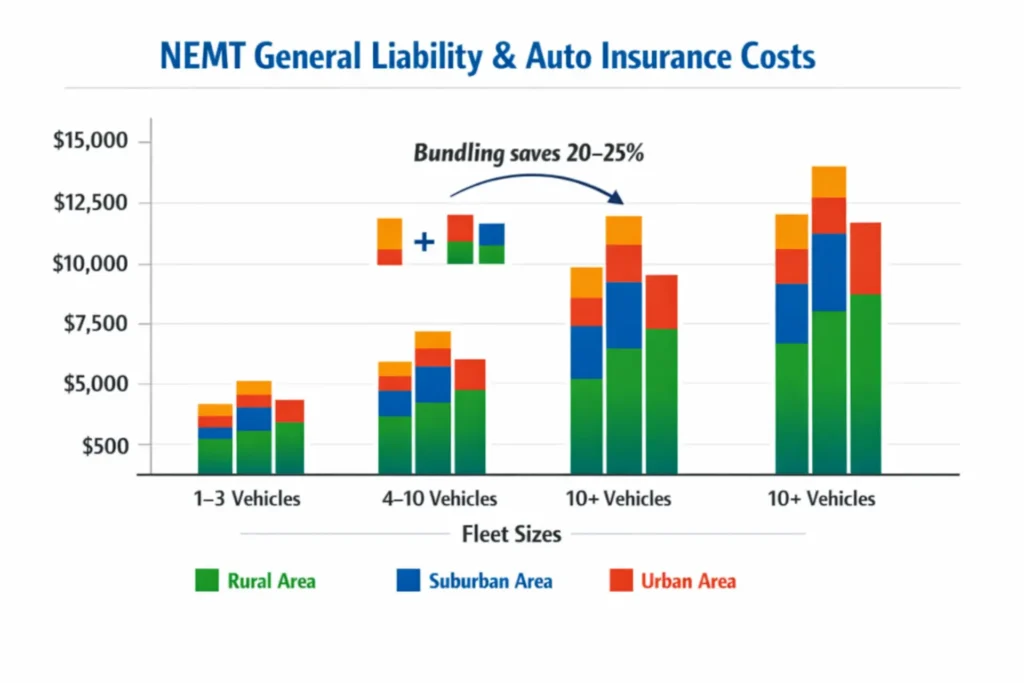

NEMT general liability insurance costs vary widely based on your operation’s size, location, and risk profile. For a small rural operator with a clean driving record, GL alone might cost $800–$1,500 per year. For a large urban fleet with a complex risk profile, that cost can easily reach $8,000–$15,000+ annually. Understanding the cost factors and bundling strategies can help you budget accurately and find legitimate ways to reduce your premium.

Annual Premium Ranges by Fleet Size and Location

A small NEMT fleet (one to three vehicles) in a rural area typically pays $800–$1,500 annually for GL coverage. Rural areas have lower claim frequency and lower medical costs, so insurers price accordingly. That same small fleet in a suburban area—a growing NEMT market—typically pays $1,200–$1,800 per year as claim frequency rises with higher population density. A small fleet operating entirely in an urban area faces the highest premiums: $1,500–$2,500 annually, reflecting the higher cost of claims and litigious environment in dense urban centers.

A medium fleet (four to ten vehicles) in a rural setting typically pays $3,200–$5,000 annually total for GL, not per vehicle. The per-vehicle cost begins to drop as insurers recognize some economies of scale. That same medium fleet in an urban area pays $5,000–$8,000 annually. The per-vehicle cost is lower than the small-fleet equivalent because insurers apply volume discounts—typically 5–15% per additional vehicle once you cross the three-vehicle threshold.

A large fleet (ten or more vehicles) typically pays $8,000–$15,000+ annually depending on location, claims history, and driver records.

For a complete breakdown of all NEMT startup costs including insurance, equipment, and licensing, consult our comprehensive startup guide.

The per-vehicle cost continues to decline, but the absolute premium rises because the aggregate exposure is higher. Volume discounts can reduce your marginal per-vehicle cost significantly, making it cheaper to add a tenth vehicle than a fourth vehicle.

Ten Factors That Directly Affect Your Premium

Your exact premium within these ranges is determined by ten specific factors. First, fleet size: more vehicles increase total exposure, but the marginal cost per vehicle drops. Second, vehicle age: vehicles older than ten years carry a 15–25% premium surcharge due to reliability concerns and repair costs. Third, driver safety record: a clean five-year record earns 10–20% discount; a single at-fault accident can trigger a 30–50% surcharge; multiple violations can make you uninsurable.

Fourth, operating radius: a small local operating radius (five to ten miles) is the baseline cost. Expanding to regional (25-mile radius) adds 5–10% to your premium. Multi-state operations add 20–40% to your baseline because insurers classify that as high-risk due to congestion, varied road conditions, and regulatory complexity. Fifth, Medicaid versus private pay mix: counterintuitively, a high Medicaid percentage can slightly reduce your premium (5–10% lower) because Medicaid is predictable and less lawsuit-prone than private pay.

Sixth, geographic location: this is one of the highest-impact factors. Operating in a high-litigation state like New York, California, or Illinois can increase your premium 30–100% compared to rural states. Urban areas within those states are worse. Seventh, coverage limits: the standard $1,000,000/$2,000,000 is your baseline. Upgrading to $2,000,000/$4,000,000 adds 15–25% to your premium. Eighth, claims history: each claim in the past three years can add 20–50% to your renewal premium. A clean five-year history can earn you 10–20% off compared to a new operator with unknown history.

Ninth, driver training and certifications: drivers with CPR, First Aid, or PASS certification earn 5–10% discounts because insurers view them as lower-risk. Tenth, customer demographics: transporting primarily elderly or disabled populations can add 5–15% to your premium due to higher injury severity and fall risk.

NEMT Insurance Cost Calculator

Estimate your annual GL and auto insurance costs based on your operation

Bundling GL with Commercial Auto Saves 20–25%

The single most impactful way to reduce your total insurance cost is bundling GL with commercial auto through the same carrier. Standalone GL costs $800–$2,500 annually. Standalone commercial auto for a small fleet costs $3,500–$6,000 annually. If you purchase them separately from different carriers, your combined annual cost is $4,300–$8,500. But if you bundle both policies with one carrier, your total annual cost drops to $4,500–$7,500—a savings of $500–$2,000 annually, or roughly 15–25%.

Here's a concrete example: You operate a three-van NEMT business in a suburban area with clean driver records. Your standalone GL quote from Carrier A is $1,400. Your standalone auto quote from Carrier B is $4,200. Total: $5,600. But a bundle quote from Carrier C for GL plus auto together is $4,600. You save $1,000 per year, or 18%. Over five years, that's $5,000—enough to purchase additional safety equipment or upgrade your fleet.

Insurers offer bundling discounts because combining GL and auto into one policy reduces their administrative overhead and improves customer retention. They're willing to sacrifice some premium to keep both your GL and auto business in-house. Always request a bundled quote from at least one carrier and compare it against your separate quotes before making a decision.

For a comprehensive breakdown of all NEMT insurance costs including both GL and commercial auto, see our detailed NEMT insurance cost guide.

Monthly Versus Annual Payment and Hidden Fees

Most NEMT GL policies are written as annual policies, but payment options vary. Annual payment (paying the full premium upfront) is the base quote. Many insurers offer a 5–10% discount for annual payment because they avoid payment-processing risk and collection costs. Monthly payment (dividing your annual premium into twelve installments) typically adds a 3–5% finance charge plus a $10–$40 monthly administrative fee. A policy that costs $1,200 annually becomes $1,260–$1,320 when paid monthly—a $60–$120 annual markup.

Beyond the premium itself, expect a one-time administrative or processing fee of $50–$150 at policy inception. Some carriers bundle this into the premium; others charge it separately. Late payment penalties (late fees of $25–$50 per occurrence) and non-payment can trigger a lapse in coverage, which causes immediate Medicaid network deactivation. Set up automatic payments to avoid this trap.

Choosing the Right General Liability Policy

Selecting a GL policy requires understanding the difference between policy types (occurrence versus claims-made), setting appropriate coverage limits, and requesting the correct endorsements for your network. Get these decisions wrong at the start, and you could face coverage gaps, claim denials, or network termination down the line.

Occurrence Versus Claims-Made Policies

An occurrence-based GL policy covers any incident that physically occurs while your policy is in force, regardless of when the claim is filed. If your occurrence policy was active on December 15, 2024, and a patient slips during a pickup on that date, your policy covers that incident even if the patient doesn't file a lawsuit until December 2026—two years after the policy ended. The coverage is tied to when the incident happened, not when the claim is reported.

A claims-made policy covers claims only if both the incident and the claim are filed while the policy is active. If your claims-made policy ends on December 31, 2024, and an incident occurs on December 15, but the patient files suit on January 15, 2025, you're uninsured. The policy didn't pay because the claim was filed after the policy expired. This seems like a minor distinction, but it creates enormous problems if you switch carriers, sell your business, or let your policy lapse.

Occurrence policies cost 15–25% more annually than claims-made policies because insurers assume greater long-tail liability—they're on the hook for future claims arising from past incidents. Claims-made policies cost less initially because insurers only pay for claims filed during the policy period. But when you eventually exit a claims-made policy (whether you're selling the business, switching carriers, or retiring), you must purchase tail coverage (extended reporting period insurance) to protect yourself for claims that might be filed after the policy ends. Tail coverage typically costs 1.5–3 times your annual premium—roughly $1,500–$3,000 for a small operator—creating a surprise cost at the worst possible time.

For NEMT operators, occurrence-based GL is strongly recommended. Most Medicaid networks implicitly expect occurrence coverage, and the modest annual premium increase (15–25%) is far outweighed by the security of not having to purchase expensive tail coverage later. If you're considering claims-made only to save money short-term, factor in the tail cost: a claims-made policy saving $300/year only makes sense if you're certain you'll never switch carriers or sell the business.

Understanding Policy Limits: Per Occurrence Versus Aggregate

Your GL policy limits are typically expressed as two numbers: $1,000,000 per occurrence / $2,000,000 aggregate. The first number—per occurrence—is the maximum your insurer will pay for any single incident, regardless of how many claimants are involved. The second number—aggregate—is the maximum your insurer will pay for all claims combined in a single policy year.

Here's why both matter: A single slip-and-fall claim can cost $950,000 in medical bills and pain-and-suffering damages. Your $1,000,000 per-occurrence limit covers it fully. But what if you have two major claims in one year? The first claim costs $1,200,000 (exceeding your $1,000,000 per-occurrence limit, leaving a $200,000 gap you cover personally). The second claim costs another $900,000. Together, those claims total $2,100,000, exceeding your $2,000,000 aggregate. Your aggregate pays up to $2,000,000 total, leaving you personally liable for $100,000 of the second claim—even though neither individual claim exceeded your per-occurrence limit.

This aggregate exhaustion scenario is uncommon for small fleets with one or two vehicles and clean claims histories, but it happens. For larger fleets or operators in high-claims areas, the risk is real. That's where umbrella insurance comes in. An umbrella policy sits above your GL and auto limits, providing excess coverage. A $1,000,000 umbrella policy typically costs $300–$800 per year and kicks in once your base GL and auto limits are exhausted. It's recommended for fleets with 10+ vehicles or for operators in high-litigation urban markets where the probability of multiple claims in one year is elevated.

Critical NEMT Endorsements and Riders

Don't assume a standard GL policy covers specialized NEMT risks. You must explicitly request and verify these four endorsements before binding your policy.

First, Hired and Non-Owned Auto (HNOA) endorsement extends your GL and auto coverage to situations where employees use personal vehicles for business purposes. If a driver uses their personal SUV to make an urgent patient pickup, HNOA ensures your GL and auto policies respond if an accident occurs. MAS Transportation requires this endorsement; it's highly recommended for all operators using 1099 contractors or employees with personal vehicles. The cost is usually bundled into your policy (no additional charge) or adds $200–$500 annually.

Second, Sexual Abuse and Molestation (SAM) rider covers allegations of abuse or misconduct during patient transport. Alivi requires this rider non-negotiably. The SAM rider typically sublimits $500,000–$1,000,000 and costs $200–$400 per year. It's essential if you transport pediatric patients, developmentally disabled populations, or high-risk psychiatric patients.

Third, Professional Liability (Errors & Omissions) endorsement covers claims of professional negligence—for example, a missed appointment that causes a patient to miss critical medical care. This is optional but recommended for mid-sized fleets or for operators servicing high-acuity populations. E&O typically costs $300–$600 annually and should be a separate line item from GL.

Fourth, Workers' Compensation Waiver is documentation stating you have no employees (only 1099 contractors) or, conversely, that all employees are covered under workers' comp. This waiver costs nothing but is essential for clarity if you're ever audited by a state labor department. Misclassifying employees as contractors can trigger massive back-pay and penalty exposure.

Before binding your policy, contact your target Medicaid networks and request a detailed list of required endorsements in writing. Provide that list to your broker and ask them to confirm in the binding authority that all required endorsements are included.

NEMT Insurance Requirements Checklist

Verify compliance with all major Medicaid networks before purchasing

Coverage Minimums

Network-Specific Requirements

Before purchasing, verify your target network's exact requirements. One missing endorsement or incorrect COI format = enrollment rejection.

| Network | GL Minimum | Max Deductible | Required Endorsements |

|---|---|---|---|

| MTM | $1M / $2M | $1,000 | Additional Insured, Loss Payee (exact COI wording required) |

| ModivCare | $1M / $2M | $2,500 | Additional Insured (claims-made allowed with tail plan) |

| MAS | $1M / $2M | $2,500 | HNOA (Hired & Non-Owned Auto) endorsement required |

| Alivi | $1M / $2M | $2,500 | SAM (Sexual Abuse & Molestation) rider ($200–$400/yr) |

Policy Type & Coverage Structure

Required Endorsements & Riders

Certificate of Insurance (COI) Verification

Broker Coordination & Verification

Post-Purchase Steps (Before Enrollment)

Ready to Get Verified?

Download this checklist, complete every item, then contact your target networks to confirm compliance.

FAQ: Common Questions About NEMT General Liability

Is General Liability Insurance Required for NEMT?

Yes, general liability insurance is mandatory for NEMT operators pursuing Medicaid contracts. All major Medicaid broker networks—MTM, ModivCare, MAS, and Alivi—require a minimum of $1,000,000 per occurrence and $2,000,000 aggregate GL coverage. Without proof of active GL, you cannot enroll as a Medicaid provider or accept trips dispatched through these networks. Network enrollment is the fastest path to NEMT revenue; skipping GL removes that option entirely.

How Much Does NEMT General Liability Cost?

For a small fleet (one to three vehicles), expect $800–$1,500 annually for GL coverage in rural areas, $1,200–$1,800 in suburban areas, and $1,500–$2,500 in urban areas. When bundled with commercial auto insurance, total coverage typically costs $4,500–$7,500 annually for a small operator. Bundling saves 20–25% compared to purchasing GL and auto separately.

What's the Difference Between Commercial Auto and General Liability?

Commercial auto insurance covers vehicle collisions, accidents, and injuries that occur while driving or as a result of vehicle operation. General liability covers non-vehicle incidents: slips, falls, property damage at facilities, and premises-related claims. Both policies work together to create comprehensive coverage. You need both because neither substitutes for the other.

Which Medicaid Networks Require General Liability?

MTM, ModivCare, MAS, and Alivi all require $1,000,000 per occurrence / $2,000,000 aggregate GL at minimum. Some networks (MAS, Alivi) require specific endorsements: MAS requires Hired & Non-Owned Auto; Alivi requires Sexual Abuse & Molestation rider. Verify requirements directly with each network before purchasing.

Do I Need GL for Private Pay Patients?

Yes. While Medicaid networks mandate GL, private pay NEMT operations face the same physical risks: slip-and-fall claims, property damage, and bodily injury lawsuits. A single claim can cost $30,000–$150,000 or more. GL protects your business assets regardless of payment source.

Can I Get GL as an Independent Contractor?

Yes, independent contractors can purchase their own $1,000,000/$2,000,000 GL policy as sole proprietors. Some networks allow contractors to be covered under a parent company's GL policy; others require contractors to carry their own insurance. Owning your own GL policy protects your personal assets if the parent company's coverage is questioned.

What Happens If I Don't Have General Liability Insurance?

Without GL, a single claim leaves you personally liable. Network contracts terminate immediately. You lose Medicaid revenue. A typical slip-and-fall claim of $50,000–$150,000 becomes your personal debt. Operating uninsured is a business-ending gamble.

How Do I File a General Liability Insurance Claim?

Contact your insurance broker immediately after an incident occurs—ideally within 24–48 hours. Provide a written incident report, photos of the scene, witness contact information, and copies of any medical bills or repair estimates. Most policies require notification within 30–60 days. Your insurer will assign an adjuster to investigate liability and manage the claim or settlement.

Does GL Cover Multiple Vehicles?

Yes, a single GL policy covers your entire fleet. The policy is based on your business operations, not individual vehicles. Your aggregate limit applies to all vehicles combined per policy year. As your fleet grows, per-vehicle cost typically decreases due to volume discounts.

How to Get General Liability Insurance for NEMT

Securing GL insurance involves selecting between specialty brokers and direct online platforms, gathering required documentation, and understanding the timeline from application to active coverage. Get this process right, and you'll be network-ready within two weeks. Rush it or skip steps, and you'll face delays or coverage gaps.

Specialty Brokers Versus Direct Online Platforms

A specialty broker understands NEMT-specific insurance requirements and can pre-align your Certificate of Insurance (COI) with MTM, ModivCare, and other network specifications. This reduces rejection risk—a COI that's missing the "Additional Insured" phrase or lists the network name incorrectly can freeze your Medicaid billing for weeks while you correct it. Specialty brokers handle that alignment proactively. The trade-off is timing: broker quotes typically take 5–7 business days from initial call to bound policy, compared to 48–72 hours for online platforms. But the compliance certainty is worth the wait.

Direct online platforms offer speed and self-service. You fill out an application, receive a quote within 24–48 hours, and can bind coverage immediately. This works well for straightforward cases: one to three vehicles, clean driver records, rural or suburban operations. But online platforms offer "one-size-fits-all" policies that often miss NEMT-specific requirements. You might discover after enrollment that your policy lacks the HNOA endorsement MAS requires, or that your COI wording doesn't match ModivCare's specifications.

For most NEMT operators, a specialty broker is worth the extra few days. The cost is the same (brokers receive commission from insurers, not from you), but the compliance confidence is higher. If you're a very small operator with a clean history and simple needs, online platforms work, but verify network requirements first.

Pre-Application Checklist: What You'll Need

Have these documents organized before contacting a broker or platform. Gathering them afterwards slows the underwriting process.

Business essentials include your EIN (Federal Employer Identification Number) or SSN if you're a sole proprietor, Articles of Incorporation or LLC formation documents, and realistic projections of annual mileage and patient trips. Fleet data includes VINs, year/make/model for each vehicle, and vehicle type (standard sedan, wheelchair-accessible van, stretcher van). Driver data includes a roster of all drivers with their names, license numbers, and—critically—three-year Motor Vehicle Records (MVRs) for each driver.

Safety and history documentation includes any insurance loss runs from the past three to five years (showing prior claims), certifications for drivers (CPR, First Aid, PASS), and your state DMV records if you're a new operator with no prior insurance history.

Create a single folder on your computer called "Insurance Vault" and collect these documents as PDFs. Having everything ready before your first broker call shaves three to five days off the underwriting process and demonstrates professionalism that sometimes influences underwriter decisions.

14-Day Timeline: From Application to Active Coverage

Day 1 and 2: Gather all documents and choose between a specialty broker and direct platform. If using a broker, call and request initial quotes.

Day 3 and 4: Submit your complete application with all documentation. Receive initial quote (ballpark pricing from underwriter).

Day 5–8: Underwriting review and follow-up. Underwriter may request clarification on driver records, revenue projections, or specific NEMT operations (for example, whether you transport bariatric patients or high-acuity psychiatric populations). Answer questions promptly to avoid delays.

Day 9 and 10: Binding authority issued. Sign the binding authority and submit payment (often via credit card or ACH). Your coverage is now effective.

Day 11: COI (Certificate of Insurance) issued. Download the COI and immediately upload it to all your target network portals: MTM, ModivCare, MAS, Alivi, and your state Medicaid agency.

Day 12–14: Networks verify receipt and activate your provider status. Trip dispatches can now begin.

Total timeline: Two weeks from first call to active coverage—assuming you have all documents ready and respond to underwriter questions within 24 hours. Delays happen if you're slow gathering documents or if the underwriter needs additional information. Planning for a two-week timeline and executing faster is better than assuming one week and facing avoidable delays.

Beyond Insurance Compliance

Secure your coverage, then let EliteMed handle your billing and revenue cycle

You've just secured your NEMT general liability insurance—a critical first step. But insurance compliance is only half the battle. To maximize your revenue and maintain steady cash flow, you need a partner managing your entire billing and revenue cycle management (RCM) process.

- Claims submission & follow-up: We submit all claims to Medicaid and private payers within 24 hours and track every claim to payment

- Network credentialing: We manage enrollment, re-credentialing, and compliance audits so you stay active with MTM, ModivCare, MAS, and Alivi

- Denial management: We appeal denied claims and recover revenue that other operators leave on the table

- Payment posting & reconciliation: We match payments to claims, identify discrepancies, and ensure 100% accuracy

- Compliance documentation: We maintain COIs, certificates, and audit-ready records so you pass every network audit

- Monthly reporting: You get clear, actionable reports on revenue, denial rates, and cash flow trends

NEMT operators who outsource billing to EliteMed see an average revenue increase of 18–25% within 90 days because we capture claims that slip through the cracks, appeal denials aggressively, and eliminate payment delays. Your drivers focus on patients. Your insurance protects you legally. EliteMed Financials handles everything in between.

Learn About NEMT Billing ServicesCommon NEMT General Liability Insurance Mistakes

Thousands of NEMT operators make preventable insurance mistakes that cost tens of thousands of dollars. Learning what to avoid saves you both money and headaches.

Mistake 1: Under-Insuring (Buying GL Without Auto)

Many NEMT startups try to save money by buying only general liability insurance, assuming it covers all risks. It doesn't. General liability excludes vehicle collisions entirely. If your van hits a parked car or injures a pedestrian, your GL policy denies the claim. You're personally liable for $30,000–$100,000 in damages, medical bills, and legal defense costs.

The solution is simple: always pair a $1,000,000+ commercial auto policy with your $1,000,000/$2,000,000 GL policy. Treat them as inseparable. Your broker can bundle them for 20–25% savings, making the combined cost only slightly more than GL alone.

Mistake 2: Choosing Lower Limits ($500K Instead of $1M)

Operators in states with lower legal auto minimums sometimes assume GL can be lower too. They buy $500,000/$1,000,000 GL to save premium. But Medicaid networks require $1,000,000/$2,000,000 minimum. A $500K policy means network rejection or deactivation if discovered during an audit. Plus, a serious slip-and-fall claim easily exceeds $500,000, leaving you personally liable for the gap.

Standardize on $1,000,000/$2,000,000 GL to remain network-ready. The modest premium difference (5–10% higher than $500K) is worth the compliance certainty.

Mistake 3: Skipping Required Endorsements (HNOA, SAM)

Forgetting to request Hired & Non-Owned Auto (HNOA) endorsement for employee-owned vehicles or failing to add Sexual Abuse & Molestation (SAM) rider means standard GL denies claims in those areas. Your driver has an accident in their personal SUV—no coverage. An accusation of misconduct arises—no coverage. Network like Alivi deactivates you immediately.

The solution: Before binding your policy, contact your target networks and request a detailed list of required endorsements in writing. Provide that list to your broker and confirm in the binding authority that all endorsements are included.

Mistake 4: Claims-Made Without Tail Coverage Planning

Cheap claims-made GL policies seem like a great deal initially—they cost 15–25% less than occurrence policies. But when you switch carriers or sell your business, you must purchase tail coverage ($1,500–$3,000) to protect yourself for claims filed after the policy ends. Operators who forget this face either an unexpected large bill or permanent uninsured exposure for past incidents.

The solution: Choose occurrence-based GL from the start—no tail needed later. The higher upfront cost (15–25%) is offset by avoiding a surprise tail bill when you exit.

Mistake 5: Not Verifying Network Requirements First

Many operators shop for the lowest price without confirming their policy meets specific network requirements. They buy a GL policy, then discover during enrollment that the COI wording is wrong, a required endorsement is missing, or the deductible exceeds network limits. The network rejects the COI. Billing freezes. Revenue stops while you scramble to correct it—a seven to fourteen day delay losing $5,000–$15,000 in trips.

The solution: Before purchasing, contact your target networks (MTM, ModivCare, MAS, Alivi) and request their current GL requirements in writing. Show that list to your broker and ask them to confirm in writing that your policy meets every requirement before you sign.

5 Common NEMT Insurance Mistakes

And How to Avoid Them

What's the problem?

Many NEMT startups try to save money by purchasing only general liability insurance, assuming it covers all their risks. They skip commercial auto because it seems expensive. This is one of the costliest mistakes you can make.

What goes wrong?

General liability explicitly excludes vehicle collisions and in-vehicle injuries. If your van hits a parked car at a medical facility, your GL policy denies the claim entirely. You're personally liable for all damages.

- Your van collides with a parked car: $30,000–$50,000 in damages

- You injure a pedestrian: $50,000–$100,000+ in medical bills and legal fees

- Your driver hits another vehicle: $100,000+ in comprehensive damages

- GL policy response: Complete denial—zero coverage

- Your responsibility: 100% out-of-pocket liability

Network impact:

All major Medicaid networks (MTM, ModivCare, MAS, Alivi) require BOTH $1M GL AND commercial auto. If they audit your coverage and find you have no auto insurance, your contract is terminated immediately. You lose all Medicaid revenue.

- Treat GL and commercial auto as inseparable—bundle them together

- Request a bundled quote ($4,500–$7,500/year) instead of separate quotes

- Bundling saves 20–25% compared to separate carriers

- Before binding any policy, confirm it meets network requirements for BOTH coverage types

- Never purchase GL without commercial auto, even to save money short-term

What's the problem?

To save a few hundred dollars annually, some operators buy GL with $500,000 per occurrence / $1,000,000 aggregate instead of the $1,000,000 / $2,000,000 that networks mandate. This creates two problems: network rejection AND personal liability for the gap.

What goes wrong?

First, you don't meet network requirements. MTM, ModivCare, MAS, and Alivi all require minimum $1M/$2M GL. A $500K policy means your Certificate of Insurance (COI) is rejected by the network. You can't enroll. Second, if a claim exceeds your $500K limit, you're personally liable for the gap.

- Serious slip-and-fall claim: $800,000 in damages and medical costs

- Your $500K policy covers: $500,000

- You pay out-of-pocket: $300,000 (the gap)

- Network discovers under-limit coverage: Immediate deactivation

- Billing freezes: Revenue stops until corrected

Why networks don't accept lower limits:

Medicaid networks set $1M/$2M minimums because slip-and-fall claims, especially involving elderly patients, frequently exceed $500K. Paying out-of-pocket for the gap puts you at bankruptcy risk, which makes networks nervous about your stability.

- Standardize on $1,000,000/$2,000,000 GL—the universal network minimum

- The premium difference between $500K and $1M is only 5–10% ($400–$600/year)

- That modest extra cost buys peace of mind and network readiness

- Never shop for lowest price; shop for the RIGHT limits first, then negotiate price

- Confirm your policy limits in writing before signing

What's the problem?

Networks like MAS and Alivi require specific endorsements—additions to your base GL policy that expand coverage. Many operators forget to request these endorsements during quoting, then discover after binding that their policy is non-compliant.

Two critical endorsements:

HNOA (Hired & Non-Owned Auto): Required by MAS. Covers your employees if they use personal vehicles for business. Without HNOA, an accident in an employee's personal SUV is uninsured.

SAM (Sexual Abuse & Molestation): Required by Alivi. Covers allegations of abuse or misconduct during transport. Without SAM, an accusation is completely uninsured, and your policy might explicitly exclude this.

What goes wrong?

- Employee uses personal vehicle for pickup: Accident occurs

- Standard GL policy denies claim (no HNOA endorsement)

- Your driver is personally liable, or you cover it out-of-pocket

- MAS audits and discovers missing HNOA: Contract terminated

- Same result with Alivi if SAM rider is missing and allegations arise

- Contact your target networks (MTM, ModivCare, MAS, Alivi) BEFORE purchasing

- Request their endorsement requirements in writing

- Provide that list to your broker and ask them to confirm in the binding authority

- HNOA usually costs nothing (bundled); SAM costs $200–$400/year

- Never bind a policy without written confirmation that all required endorsements are included

What's the problem?

Claims-made GL policies cost 15–25% less than occurrence policies. To save money, some operators buy claims-made. But when they switch carriers or sell the business years later, they face an unexpected bill for tail coverage: $1,500–$3,000+.

How claims-made works:

A claims-made policy covers claims ONLY if the incident AND the claim both happen while the policy is active. If your policy ends on December 31, and a patient files suit on January 15 for an incident from December, you're uninsured.

When you exit (sell the business, retire, switch carriers), you must buy tail coverage—extended reporting period insurance—that extends coverage for claims filed after the policy ends. Tail typically costs 1.5–3 times your annual premium.

What goes wrong?

- Year 1–5: Pay cheap claims-made premiums ($900/year vs. $1,200 occurrence)

- Year 6: Sell your business or retire

- Tail coverage quote arrives: $1,500–$3,000 (surprise bill)

- You either pay the unexpected cost or accept a permanent coverage gap

- If a lawsuit is filed years later, you're completely uninsured

- Choose occurrence-based GL from day one (only 15–25% higher premium)

- Occurrence covers incidents whenever they occur, with no tail needed later

- If choosing claims-made, set aside $1,500–$3,000 now for future tail coverage

- Ask your broker in writing about tail cost and timeline before binding

- Understand that with claims-made, the true cost = annual premium + eventual tail bill

What's the problem?

Many operators shop for the cheapest GL quote without verifying their policy meets their target network's exact requirements. They buy a policy, then discover during enrollment that the COI wording is wrong, a required endorsement is missing, or the deductible exceeds the network's limit.

What goes wrong?

- You buy GL policy without checking MTM requirements first

- MTM's enrollment portal rejects your COI (wrong format or missing Additional Insured designation)

- Your enrollment is halted; you can't accept trips

- Revenue stops—7–14 day freeze while you scramble to fix the policy

- You contact your broker, request amended COI, wait for reissuance

- Resubmit to MTM; wait 3–5 days for approval

- Total delay: 10–14 days = $5,000–$15,000 in lost trip revenue

Network COI wording differences:

MTM's COI wording is different from ModivCare's. MAS requires specific language. Alivi requires different designation. One certificate doesn't fit all networks. A mismatched COI means rejection.

- Contact MTM, ModivCare, MAS, and Alivi BEFORE purchasing any policy

- Request their current GL requirements and COI format in writing

- Share these requirements with your broker and ask for written confirmation

- Request a sample COI draft BEFORE binding to verify format accuracy

- Only bind the policy after the broker confirms all network specs are met

- Have the broker note any network-specific COI formatting in the binding authority

These five mistakes are 100% preventable. Before you purchase any general liability policy, verify network requirements in writing, confirm your broker meets every spec, get a COI draft for review, and don't bind until you're certain the policy is compliant. Spending an extra week on verification saves you from $5,000–$300,000 in potential losses.

Download This Mistakes Guide

Print this guide and walk through each section with your insurance broker to ensure you don't make any of these common errors.

Conclusion and Next Steps

NEMT general liability insurance is not optional—it's legally mandated by Medicaid networks, financially essential for protecting your business from claims that can reach six figures, and a basic operating requirement for any NEMT provider.

For a comprehensive roadmap to launching an NEMT business with full insurance and network compliance, see our complete guide to starting an NEMT business.

Understanding what GL covers, why you need both GL and commercial auto, what networks require, how much it costs, and how to avoid common mistakes positions you to make confident purchasing decisions.

Your next step is straightforward. Contact a NEMT-specialty insurance broker (recommended) or visit a direct platform. Provide the documentation checklist outlined in this guide. Request quotes that comply with your target networks' requirements. Compare bundled GL plus auto quotes against separate quotes and choose the option with the greatest savings. Bind your policy, download your COI, and upload it to your networks' portals.

Secure Insurance, Capture Leads

Pair your NEMT general liability coverage with a professional website built for Medicaid networks

Insurance compliance is essential, but it won't bring patients to your door. NEMT brokers and dispatch networks receive hundreds of applications annually from operators with identical insurance coverage. What separates the operators who scale to 20+ vehicles from those stuck at three vehicles? A professional, network-ready website.

- Network-compliant design: Built to meet MTM, ModivCare, MAS, and Alivi specifications for provider directory visibility

- SEO-optimized content: Rank for NEMT searches in your service area, capturing local patient leads 24/7

- Lead capture forms: Collect patient inquiries, dispatch vendor contacts, and insurance broker referrals directly on your site

- Mobile-first responsiveness: 85% of NEMT searches happen on mobile—your site must work perfectly on every device

- Trust signals: Insurance badges, certifications, testimonials, and compliance documentation build credibility with brokers and patients

- Ongoing optimization: Monthly SEO updates and A/B testing ensure your site captures every potential lead in your market

NEMT operators with professional websites see 40–60% more network applications and 20–30% faster enrollment because brokers perceive them as established, compliant businesses. Your website works 24/7 to attract and pre-qualify patients while you focus on operations.

Explore NEMT Website DevelopmentIf you need guidance selecting the right broker, verifying network requirements, or ensuring your policy meets compliance standards, EliteMed Financials offers free policy reviews and broker consultation for NEMT operators. We specialize in helping operators navigate insurance compliance so they can focus on growing their business.

Insurance Alone Isn't Enough

Your general liability covers claims. Medical billing maximizes your revenue.

General liability insurance protects you from legal and financial exposure. But it doesn't generate revenue. To build a sustainable NEMT business, you need both protection and optimization. EliteMed Financials handles the billing complexity so you can focus on growing.

- Claims scrubbing: We verify every claim before submission, catching errors that payers use to deny payment

- Real-time tracking: Dashboard access to claim status, payment dates, and aging AR so you're never in the dark

- Denial analysis: We identify denial patterns and fix coding, compliance, or documentation issues so they don't repeat

- Compliance audits: We ensure your documentation meets Medicaid and insurance payer standards, reducing audit risk

- Revenue maximization: We code services correctly, identify all billable items, and pursue every valid claim to payment

- Integrated reporting: Monthly KPI reports showing collections, aging, denial rates, and cash flow trends

Our medical billing clients see an average revenue increase of 18–25% within 90 days. We handle the administrative work that typically costs a full-time billing staff ($35K–$50K+ annually), and our fees are percentage-based—we succeed only when you succeed.

Explore Medical Billing ServicesThe investment in general liability insurance—typically $1,000–$2,500 annually for GL alone—is the single most important risk management decision you'll make. A single uninsured claim can cost $100,000+ and bankrupt a small operation. Insurance costs a few thousand dollars per year. Going uninsured gambles with your entire business.

Get insured. Get compliant. Get billing. Contact EliteMed Financials today for a free consultation.

Additional Resources

For official state Medicaid transportation requirements and coverage guidelines, visit the official Medicaid Transportation Services page.

For comprehensive information on commercial general liability insurance standards and definitions, refer to the Insurance Information Institute (III) general liability coverage resources.